It’s no surprise that inflation is getting its dirty little fingers into everything these days. Chip shortages, supply chain issues, OPEC…the list goes on and on. With a global economy comes global issues, and right now, it’s pretty painful. Even groceries now cost more than a short time ago.

So how is inflation hitting workers’ comp, and more importantly, what are some things we can do to mitigate the rise in the costs of doing business? According to Risk Management Magazine, 38% of all middle market company leaders cite inflation as their primary concern in a survey by Chubb and the National Center for the Middle Market.

So What is Really Causing All of This?

If you are up on what has caused the inflationary environment we live in right now, feel free to jump to the next section.

To understand how we arrived at this juncture, where inflation seems to be running rampant, we have to jump back several years. It’s valuable to look at the housing market and interest rates to gain a better understanding of inflation and what those trends seem to be doing.

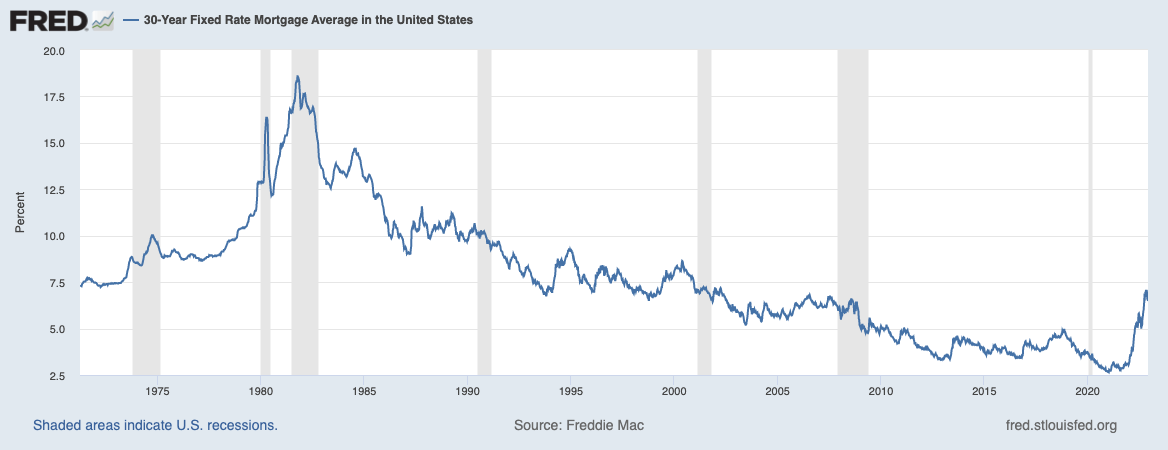

We aren’t jumping back to the 1980s when interest rates were approaching 19% on a 30-year fixed-rate mortgage due to out-of-control oil prices, government overspending, and the vicious cycle that is higher prices leading to higher wages leading to higher prices (which some economists note we are heading toward now) that started in the 1970s. There are some similarities there about what we’re seeing now, but the difference lies in what led up to these spikes.

Rewind to 2013 when we started seeing interest rates reach all-new lows in the 3% range. This was preceded by multiple rounds of quantitative easing starting in 2008. Borrowing money was cheap and largely subsidized by volume coupled with a subprime lending model. This set us on a course for the next eight or so years, but a storm was brewing.

To get a visual of what this has looked like, take a look at this graph from Freddie Mac.

Money was cheap for a long time, but corrections were on the way.

For some perspective, according to Standford economist John Taylor, inflation “jumped from 1.4% in the 12-month period from January 2020 to January 2021 to 9.1% in the 12-month period from June 2021 to June 2022.” He also sheds light on the fact that most misunderstand that one of the key drivers of inflation is the artificially low federal fund rate (the overnight bank-to-bank borrowing rate) that has been kept low for too long. Sitting in the low 2% range (at the time of this writing), the discrepancy between it and the 7-8% 30-year mortgage rate doesn’t bode well for the average consumer and is a leading indicator of things to come.

As markets do, the housing market started to correct itself. Its catalyst? The Covid pandemic and the ensuing home-buying frenzy that was set into motion. At first, when the pandemic was “new” and everyone started the process of learning how to work from home, rates stayed low…then boredom hit. People started the work-from-home shift and got bored with where they lived; it really is that simple. So we all started buying new homes. It was dog-eat-dog in the housing market. A correction was bound to happen.

Covid provided for the perfect storm to ensue. Coupled with the war in Ukraine, supply lines were stressed (and they still are to an extent) and in some cases, completely choked off. We’re still feeling that stress now.

Oil companies, largely with the help of OPEC, have posted record profits. According to PBS.org, ExxonMobil posted profits of nearly $20 billion, Chevron banked more than $11 billion, Shell had $9.5 billion, and BP made over $8 billion. Saudi Aramco, the world’s largest oil company, posted $42 billion in profit.

That was all in Q3 of 2022.

President Biden has called this a “windfall of war” as Ukraine still struggles with its battle to stay sovereign against Russia. He has called on OPEC to increase production in the wake of the organization cutting the number of barrels produced per day to put the supply/demand curve back in consumers’ favor. Russia, being a large oil producer with new sanctions put in place, has also furthered the pump prices. Supply and demand aren’t really working in our favor. The war has had a huge impact on global energy markets, and as you’ll see later, could have lasting impacts on the inflated nature of our economy.

All of this has placed stress on everything we consume. It’s now more expensive to produce and transport nearly everything. This all rolls downhill to consumers. We’re all paying the price, and much of that happens each time we drive.

It’s also worth noting that inflation isn’t unique to the US (9.1%). The United Kingdom has been looking at a 10.1% inflation rate, and Turkey has been dealing with a 79.6% inflation rate according to Forbes.

What Impact is This Likely to Have on Workers’ Comp?

Many industry experts don’t expect inflation to have a massive impact on the costs associated with workers’ comp insurance. The reasons for this are many, but they provide an optimistic outlook on what this means for insurers and consumers alike.

According to this article, premiums are actually staying stable for several reasons: “…due to several years of favorable experience, NCCI’s [National Council on Compensation Insurance] filed loss costs have generally gone down in the last few years, minimizing upward pressure on premiums,” said Barry Lipton, practice leader and senior actuary at NCCI. The National Association of Social Insurance (NASI) supports this assertion stating that premiums per $100 of insured payroll are at a 20-year minimum. “So, while wage inflation is very impactful to workers’ comp benefits and premium, the impact is benign as benefits keep up with inflation and premium stays in balance with benefits automatically,” said Lipton.

Another interesting point: among the rising wages and benefits for workers on the ground, we’re see that higher-paid workers end up being safer workers. They make fewer errors resulting in claims. That being said, wage growth is usually looked at as a favorable thing with regard to workers’ compensation insurance based on these tertiary benefits.

What’s more is that the Federal Reserve Bank of New York recently did a survey and found that median inflation rates for next year (2023) and three years from now are expected to fall; this has eased the idea that we’re in this for the long haul.

This doesn’t mean you shouldn’t watch your claims costs and how they’re riding the wave inflation is causing. Fewer claims are great, but that doesn’t underscore the fact that it’s still more expensive to recover per claim. Materials costs are up, medical costs are up, and vehicle costs are up — these are all a recipe for increased payouts if claims go up.

With all this in mind, McKinsey and Company have found three likely situations to play out in the next three years. We’ll start with the best situation and move to the less preferable. (As you know, this is all speculation; no one can see the future, but based on what is going on now, many think these three options are viable moving forward.)

First, an optimistic look toward stabilization. In this scenario, energy, food, and commodity markets would stabilize market-wide, and the Fed would most likely continue on its path of raising policy rates by 3-4% with inflation rates most likely receding in 2023. “For insurers, this is likely to represent a near-term erosion in combined ratios (losses and expenses in relation to total collected premiums) and overall profitability, but with an ultimate return to long-term norms. This scenario favors carriers with large and diversified portfolios, healthy surpluses, and operational excellence, particularly in expense and claims management.”

Next would be continued disruption. If the war in Ukraine and Covid continue to put pressure on market forces, disruption will likely continue. Commodities and energy prices will remain in flux and create unease regarding inflation; this will most likely force the Fed to bring policy rates above four percent with some estimates suggesting it being well above four. “For insurers, this scenario would translate into more persistent profitability challenges—a worse scenario than one with consistently higher inflation. Claims costs would continue to rise because of disruptions in global commodity markets, but moderate general inflation could prevent insurers from increasing premiums for customers. The result could be a severe contraction in underwriting capacity and a hard market with more stringent underwriting standards. Insurers that come out ahead will be those with superior underwriting and pricing discipline and a focus on profitable pockets of the market.” This would be bad for both consumers and insurers.

Lastly, we could see persistently elevated inflation. Here, we could see energy and commodity prices facing long-term inflated rates. In this scenario, the Fed may not be able to hike rates to a point that helps bring inflation back down. This could lead to a prolonged phase of stagflation which is marked by high interest rates that won’t budge and an imbalance in economic growth. “For insurers, this scenario would cause significant short-term disruption in combined ratios and underwriting profit. However, as sometimes happens in foreign markets with persistently high inflation, the long-term outlook might permit premiums and investment returns to rise at the same pace as expenses and loss costs. This market will favor P&C carriers that can bring operational excellence to the entire value chain, especially those with better pricing strategies and underwriting discipline.” This scenario is still considered unlikely.

Key Takeaways

In all likelihood, and according to these sources, inflation probably will have a minimal impact on P&C insurance, which contains workers’ comp. Market factors seem not to point directly at this vertical, but that doesn’t mean it’s bulletproof. Caution should be exercised in these uncertain times. In the three scenarios above, pay special attention to the bolded areas. It can’t hurt to be prepared if the worst is to happen.