Before you begin working with a contractor or other third party, it’s important to make sure that they’re not bringing any extra financial risk to your business.

Of course, every new third party that you employ creates a new layer of risk for your company – unless they’re properly insured. Therefore, it’s a common business practice for companies to acquire evidence of all third parties’ insurance coverage (relevant to the job, of course).

Follow along in one of our new additions to our Certificate of Insurance 101 guides, where we explain what a COI is and what it means in business.

Proof of insurance coverage can be provided in a couple of ways. They could carry their insurance policy around with them or make copies of it to distribute to vendors. This would be lengthy, inconvenient, and provide way more details than what you, as the business attempting to employ them, need. The other option is a certificate of insurance.

A certificate of insurance, also commonly referred to as an insurance certificate or COI, is a summarized version of an insurance policy. It’s an official legal document generated by a third party’s insurer that provides the information you need when it comes to ensuring third-party protections.

We also answer common questions that come up regarding insurance certificates and walk through some examples, so you have a better idea of when and why you’d need to know the details and when you can pass them off to someone else. Let’s dive in.

Why Do Companies Ask For Certificates of Insurance?

Now that we’ve covered what a certificate of insurance is, let’s talk about when and why businesses actually need them. Companies typically ask for certificates of insurance for two major reasons:

- To verify that a third party they’re hiring has the correct insurance in place to do a job.

- To shield their business from unnecessary financial hardship in the event of an incident that could become a claim.

Both of these boil down to protecting your business from risk.

For the former, companies must ensure that the third parties they’re working with are properly licensed and insured. Some industries even require it, such as subcontractors in construction. By requesting a COI, companies can verify that their vendors and contractors have the necessary coverage to meet any legal and regulatory requirements.

For the latter, it’s important to mitigate risks for your business and avoid extraneous expenses like litigation stemming from claims. Limiting your liability exposure by requiring that contractors and vendors have adequate insurance coverage in place is a great way to stay protected. It also helps businesses get their projects completed on time and within budget when they don’t have to worry about unforeseen costs or delays associated with accidents.

Let’s pretend that you’re employed at a construction company as a hiring and compliance manager. It’s your responsibility to ensure that all hired subcontractors have the necessary insurance coverage to protect your business from potential liability that could lead to costly litigation. This is a point where you, as the person in charge of COI compliance, would need to ask all subcontractors wanting to work for your company for a certificate of insurance.

What Does an Insurance Certificate Mean in Business?

A certificate of insurance, or COI, is a document frequently used in business transactions. The purpose of a COI is to provide evidence of an insurance policy supplied by an insurance company, typically to ensure that a vendor that you’d like to work with has active, adequate coverage in place.

For contractors, a COI is often understood to be a prerequisite for working with a business and can even be a part of the process of bidding for a job. In some industries, such as construction, COIs are more than just commonplace—they’re required. It’s especially important in these high-risk sectors to confirm the coverage of those who could get hurt and be held responsible.

For a business, insurance coverage of vendors is critical, and COIs are an easy way to verify insurance coverage and to ensure that a hired party has the insurance coverage that they say they do, in the amount and specifics that you require of them.

To put it simply, requesting and obtaining COIs is an essential business practice whenever you engage a third-party vendor’s services, whether it’s subcontractors, suppliers, equipment rental companies, or other kinds of service providers across industries.

What Is the Difference Between a Policy and a COI?

Over the course of this article, we have used the terms “insurance coverage” and “insurance certificate.” While closely related concepts, they are not the same thing.

Insurance coverage provides financial protection to whoever purchases it by way of the insured paying premiums to the insurer and the insurer agreeing to pay for financial losses that the insured may incur due to covered events. A policy is a legal contract between a policyholder and an insurer that outlines the terms and conditions of that coverage.

Policies define things such as:

- Risks covered

- Exclusions

- Deductibles

- Limits of liability

- Premiums

Certificates of insurance, on the other hand, are documents that showcase proof of insurance coverage (in other words, proof that someone is currently covered by an insurance policy). COIs are usually issued by an insurance company at a policyholder’s request to provide evidence to an entity that they are correctly insured.

COIs outline things such as:

- Policyholder’s name and contact information

- Certificate holder (requester)’s name

- Policy number

- Effective dates of coverage

- Type of coverage provided

So, a policy is the set of rules that an insurance company follows to protect a vendor, whereas a certificate of insurance is a special document that proves that they have insurance.

They work together because a policy tells the policyholder and the insurance company what they’re responsible for doing in the case of a covered incident, and a related COI proves that a policyholder has the insurance coverage that they claim to.

Let’s go back to the example where you’re a hiring manager for a construction business. You wouldn’t need (or want) to go collect actual insurance policies from all of your contractors, subcontractors, suppliers, vendors, and other hired third parties. You’d simply send them a request for a COI, which each third party would have to procure from their insurer and then provide you with their certificate. You’d then verify the COI to ensure that it meets your business’s or project’s needs, and voilà, the work can begin!

Is a Certificate of Insurance the Same as an Insurance Policy or Insurance Coverage?

Let’s clarify some important points about COIs here. Insurance certificates are similar to insurance policies, but not the same thing.

Insurance policies are:

- Issued by an insurance provider (and only valid when done so).

- Paid for in the form of premiums.

- Lengthy documents that provide every detail of the insurance coverage provided.

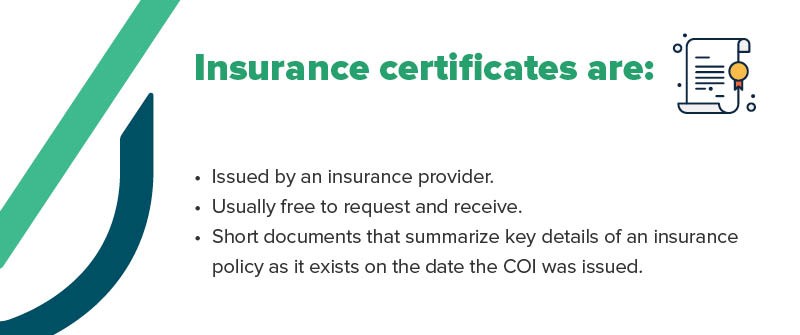

Insurance certificates are:

- Issued by an insurance provider (and only valid when done so).

- Usually free to request and receive (since someone is already paying for a corresponding policy).

- Short documents that summarize key details of an insurance policy (that act as evidence of said policy) as it exists on the date the COI was issued.

So, someone could have a general liability insurance policy and not have a COI, but a COI necessitates the existence of an insurance policy for it to provide proof.

Is a Certificate of Insurance the Same as a Declaration Page?

COIs are also not the same thing as declaration pages (also known as “dec pages”).

Declaration pages are:

- Summaries of insurance policies (including who is insured, what is insured, the type of coverage, the term of the policy, how the claim will be paid, and the premiums charged).

- A part of insurance policies (actually included as the first page of a policy’s documentation).

- Internal-facing documents (for policyholders to use to reference their coverage).

Insurance certificates are:

- Summaries of insurance policies (including who is insured, what is insured, the type of coverage, the terms and limits of the policy, names of additional insured parties, and name of certificate holder).

- Separate from insurance policies (generated as completely different documents).

- External-facing documents (provided to a hiring party who becomes known as a certificate holder)

Why Would a Business Request a Certificate of Insurance for Liability Insurance?

There are numerous reasons that a business would want to request a COI from their third-party hires. Let’s cover five big ones:

- Verification of insurance coverage. This is the primary purpose of a COI, to ensure that a vendor has documented evidence of the relevant insurance coverage they have in place. You don’t want an uninsured worker on the job, for their sake and yours.

- Risk maintenance. By requesting COIs from the third parties you work with, you shift a portion of the potential liability from your business to the vendor’s insurance carrier, reducing the risk of potential legal complications.

- Financial protection. Relatedly, by pushing potential liability to your vendor’s insurance provider, your business will not be held responsible for unnecessary costs associated with damages and uninsured claims that could come up.

- State and regulatory guidelines. As you well know, there are various governing bodies that regulate business dealings. Some states and industries have specific guidelines that you must meet, including insurance verification, to ensure your compliance.

- Due diligence. Finally, it is simply a business best practice to check in on your vendors’ insurance coverage status. Even if they are insured as they should be, it is your due diligence to ensure that their coverage is valid, current and meets your needs.

What Is a Certificate Holder on Business Insurance?

One of the details included in a certificate of insurance for business is the party it’ll be delivered to, also known as the certificate holder.

Essentially, the hiring party or whoever makes the official request for an insurance certificate (the entity that intends to verify someone’s coverage) will be officially listed on the certificate itself as the certificate holder.

What Does Insurance Certificate Mean in Business Example?

Let’s say that you are a hiring and compliance manager for a construction project. In order to meet state and industry-wide requirements, financially protect yourself and your workers from unnecessary costs stemming from damages, and do your due diligence, you should ask all hired subcontractors for a COI.

When should you do this? As soon as possible. To be more specific: certainly before they begin their work on the project, and perhaps even as a requirement for them to bid on the job.

Now, let’s say that some property damage occurs while the contractors and subcontractors are at work. Without insurance verification via COIs, your business would have been left on the hook for the damages. What’s more, you could be hit with all kinds of claims and litigation. All of these are, thankfully, avoided due to your foresight in requesting and verifying the insurance of your workers.

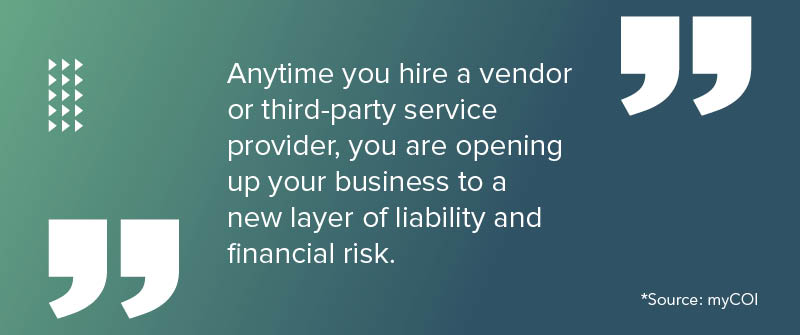

When Do You Need a Certificate of Insurance From a Vendor?

Anytime you hire a vendor or third-party service provider, you are opening up your business to a new layer of liability and financial risk. For this reason, you should always make it a priority to send them a COI request with your specific requirements laid out so that they can ensure contractual compliance.

You should aim to get a certificate of insurance from a vendor as soon as possible, and at the very least, before they begin working with you on a job and exposing your business to risk.

Can I Issue My Own Certificate of Insurance?

You cannot issue your own certificate of insurance, and neither can your vendors. Only the insurance agent or broker providing someone with a policy can confirm its existence and issue a corresponding certificate proving it. However, while an insured cannot issue their own certificate of insurance, obtaining a COI from their insurer is typically a quick, simple, and free process.

How to Get an Insurance Certificate Online

Now that we’ve covered the important note that you cannot issue your own insurance certificate, you may be wondering if it’s possible to get a business certificate of insurance online at all.

For contractors attempting to get a COI in hand for their own coverage to present to the business intending to hire them, if their insurance provider has some kind of online portal, they can take steps virtually to receive their certificate.

For businesses or contractors attempting to gain a better understanding of the way COIs work, a database of free business certificates of insurance examples and samples is available online here.

How to Manage and Track COIs

We’ve covered many details inherent to the COI management process here. The most important steps are the first few—the requesting and obtaining of insurance certificates from relevant vendors—but the process doesn’t stop there.

Prudent businesses should continue through this certificate of insurance timeline by verifying that a COI meets their vendor requirements, keeping the document on file for at least five years for their records, and noting the dates of its expiration to reach out in time for its renewal.

Managing COIs from various vendors can get difficult quickly, especially as your vendor network scales. There are many steps involved in this compliance process, and it’s understandable if you don’t feel like (or don’t want to become) an insurance compliance expert.

A growing number of businesses are smartly outsourcing their COI management efforts to COI tracking software platforms that help streamline and vet the process as they go along, freeing up their time and granting them peace of mind.

We Have Your Business’ COI Needs Covered

If you would like additional assistance with managing COIs from various third parties, myCOI’s software can help. Our sophisticated but easy-to-use platform simplifies insurance tracking by providing your company with a solution to automate insurance certificate requests, collection, and compliance resolution. Say goodbye to time spent manually requesting, tracking, and managing COIs, and say hello to more time spent doing work you’re passionate about.