When attending a big event, you want to dress the part. The same rule applies to risk management. Organizations well prepared for combatting loss events have their “risk bowtie” ready to go. The bowtie method provides a model for thinking about potential risks and their impact on a company. The diagram helps businesses prioritize likely hazards and put processes in place to minimize both their likelihood of occurring and the business effects when they do. In this article, we discuss the five parts of the bowtie method and how to make it work for risk mitigation.

The Bowtie Method for Risk Management: A Deeper Dive

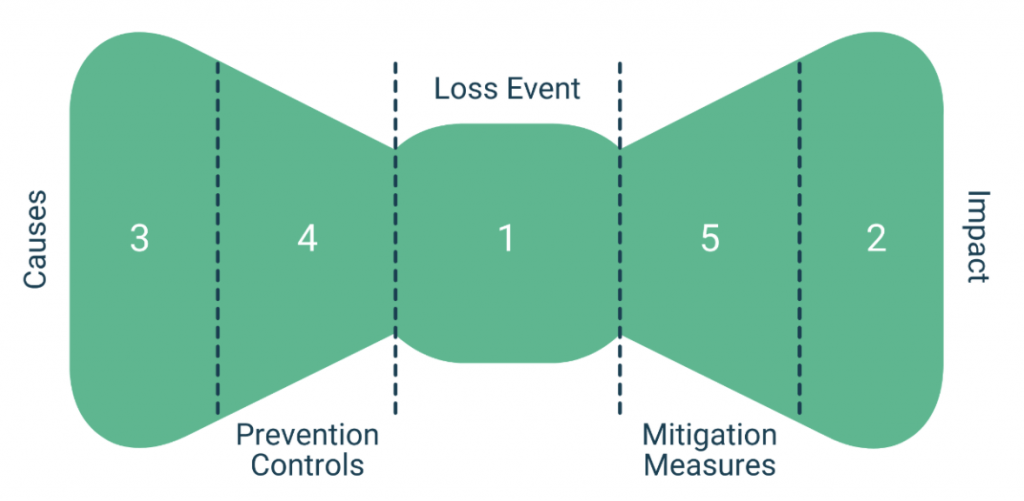

Bowtie diagrams are a visual exercise for identifying and analyzing risk pathways from cause to consequence. The left side captures proactive methods to prevent risk triggers. The right side holds reactive measures to adequately respond to losses and lessen their magnitude.

The model makes understanding risk easier throughout a company and prompts preemptive decision-making. By prioritizing risks and the factors that create them, leadership can craft appropriate mitigation plans. The more risk is anticipated and prepared for, the more it can be avoided.

Let’s put the bowtie method to work using the scenario of a property management company for a multi-unit retail space.

Step 1: Identify the Risks

Start by identifying the risk and its likelihood of occurring. Pair the chance of a risk becoming a reality with its effects in step two for setting management priorities.

We isolate fire as a key property risk. Its odds of happening depend on a range of factors like the age of our building, construction materials used, types of occupants, nearby building proximities, distance to the nearest fire station, etc.

Step 2: Assess the Effects

The next step is documenting the consequences of a fire on our property. Here we build the business case for managing the risk.

We find that such an event could include out-of-pocket repair costs and loss of income if the property becomes non-functional. Costly litigation for breach of contract and medical injury of occupants is possible. Our company would be liable if the fire reached other nearby buildings. A major fire could significantly impact our insurance loss history and raise premiums across the next five years.

Step 3: Isolate the Causes

These are the threats likely to trigger the risk. Causes of an event can be direct or indirect and should be specific.

Our analysis shows we lease to several restaurants all preparing food with large industrial ovens, gas stoves, and fryers. The property was built before the city’s new fire ordinances and therefore is operating with some exemptions. We do not trust the maintenance records for fire extinguisher recharges and sprinkler tests. Patrons frequently ignore fire zones in our parking lot designated exclusively for hydrant and water line access.

Step 4: Create Prevention Controls

This step works to make potential risks improbable realities. Here we put barriers in place intended to stop the threat. Many of these controls may be physical actions around the property. However, prevention controls also should include contractual risk transfer strategies.

We bring our building into compliance with the latest fire ordinance and institute a key performance metric program for the maintenance staff designed to prevent losses. After a legal review of our lease agreement, we add an indemnification clause and require an additional insured endorsement from all tenants for an added layer of financial protection.

Step 5: Develop Mitigation Measures

Response and recovery strategies are the final steps in the bowtie method. Unfortunately, no business is ever risk-free. However, risks become more acceptable when they are addressable. Mitigation measures expedite a company’s ability to react and lessen the impact of a loss event. Insurance covering the property and its tenants represents one of the most important reactive measures available.

To minimize potential fire damage, we improve emergency signage and instructions throughout the property. We also increase the coverage amount of our general liability insurance policy and require leasees to do the same. Automated certificate of insurance (COI) tracking for every tenant becomes a hallmark of our risk management strategy to ensure every occupant is insured and contract compliant throughout their lease.

Tie Up Loose Ends with myCOI

For your next loss event, will your company be dressed for success? Now is the time to start planning. Reach out to myCOI and learn how our automated certificate of insurance tracking software and team of insurance experts keep clients risk-ready and in control.