In the process of hiring a new vendor, you review their certificate of insurance (COI) to make sure your company is covered against a potential loss:

- The Commercial General Liability (CGL) policy is active and coverage amounts are ample for the project’s value.

- The vendor has workers’ compensation insurance.

- The COI cites your company as an additional insured.

Everything is good to go, right? Not so fast. A liability cap may be hiding in plain sight known as the “general aggregate limit.” Understanding when this limit takes effect can mean the difference between a vendor having coverage or being underinsured. This article details the three different applications of the general aggregate limit and some common pitfalls that impact coverage.

What is the General Aggregate Limit?

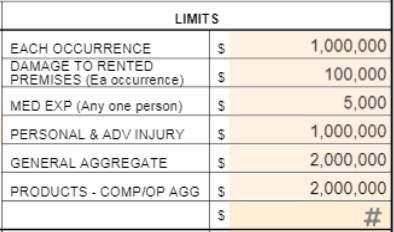

CGL insurance policies carry liability limits, which means that during the term of coverage, the insurance will pay only up to a certain amount. Once the policy reaches those thresholds, its financial resources are exhausted. Two important limits include “each occurrence” and “general aggregate”:

Each occurrence is the maximum amount a policy pays for an individual claim. Using our example limits, this policy pays up to $1 million for a single claim but cannot exceed that amount. Overages must go toward an umbrella or excess insurance policy or result in out-of-pocket costs.

General aggregate represents the maximum amount a policy pays out across all claims. After paying $1 million for the example claim above, the policy still has $1 million remaining to cover any additional claims during the coverage term.

When do General Aggregate Limits Apply?

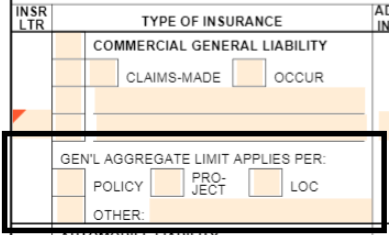

Understanding how limits impact payouts is step one. Next is knowing when the limits apply. This information comes from the three boxes under “General Aggregate Limit Applies Per” on the COI.

Policy indicates that the limits apply to the insurance policy in total. A vendor may work on several projects at once for different companies under the same policy. Should the vendor cause losses at different worksites, all claims go against the general aggregate as a whole. After reaching $2 million, the policy stops paying. Companies filing claims after the aggregate is reached likely will not receive payment.

Project applies the liability limits to each job rather than the entire policy. Therefore, our vendor would have $2 million in coverage for each project. If the vendor did five projects per year, they have a policy aggregate of $10 million in coverage. Project is a preferred general aggregate for hiring companies because it provides a higher coverage threshold and more control over that money. Should another company file a claim against the vendor’s policy, the amount of that claim would have no bearing on how much the policy would pay against any other losses filed under a separate project.

Location applies only to the properties owned or rented by the policyholder. This aggregate limit has no application for a company hiring a vendor because it excludes worksite locations. The location limit is designed only for the named insured’s properties like office buildings, retail locations, and equipment storage facilities.

What are Some General Aggregate Limit Pitfalls?

- Know how courts define an occurrence – Courts are divided in what constitutes an occurrence. Let’s say our vendor is an electrician whose faulty work causes a fire injuring 20 patrons. Some state courts apply the “cause test,” which views the liability cause as the faulty wiring. This equals one occurrence. Other state courts apply the “effect test.” This method defines the occurrence by the resulting damage or injury. In this case, the court considers each injured patron a separate occurrence for 20 total claims.

- Check for project aggregate endorsements – Simply checking the project aggregate limit box on the COI does not mean the coverage exists. Per project is not standard and often comes with an additional premium cost. The CGL policy requires a per-project aggregate endorsement that should be attached to the COI upon submission to verify accurate coverage.

- Beware CGL policy extensions – Policyholders sometimes seek to extend their policies for longer than the standard 12 months but less than an additional full term. Perhaps a project will last 15 months, so a vendor gets a three-month extension of their CGL policy. Know that when this happens, the aggregate limits do not reset at the 12-month mark. The aggregate extends for the 15 months increasing the likelihood that the amount could be exhausted. Note the effective and expiration dates of the policy on the COI to identify this potential issue.

Do not Let General Aggregates Limit Your Project Protections

Certificates of insurance provide valuable details to keep your company covered against third-party risks. For more insider advice on leveraging COIs, download our eBook “8 Tips to Review a Cert Like an Insurance Pro.”

If your business could benefit from an automated system for tracking and managing certificates of insurance, schedule a demo with myCOI. Our platform is built on industry logic and supported by insurance experts. The software tracks each important detail of COIs to keep your company safe. When it comes to risk, we erase the worry and save time so you can get back to work.