Best Certificate of Insurance Tracking Software

Protect Your Business From Costly Claims

Ask your CFO or Risk Manager just how much claims and lawsuits can cost your business. If you are collecting certificates just to confirm they were received, you have no guarantee that your requirements are being met. myCOI Central is built on a foundation of insurance industry logic to ensure you remain protected with the appropriate coverage.

Automate Your COI Tracking

There’s no more need to worry about stacks of certificates cluttering up your office or hours of frustrating phone calls and emails to chase down certificates. myCOI Central provides your company with a solution to automate your insurance certificate requests, collection, and compliance resolution, while also giving your team a single, centralized repository to view compliance.

For Agents & Brokers

Win business and boost retention by providing agency branded, industry leading insurance tracking software to your insureds. Offer software only or add on your own compliance review services.

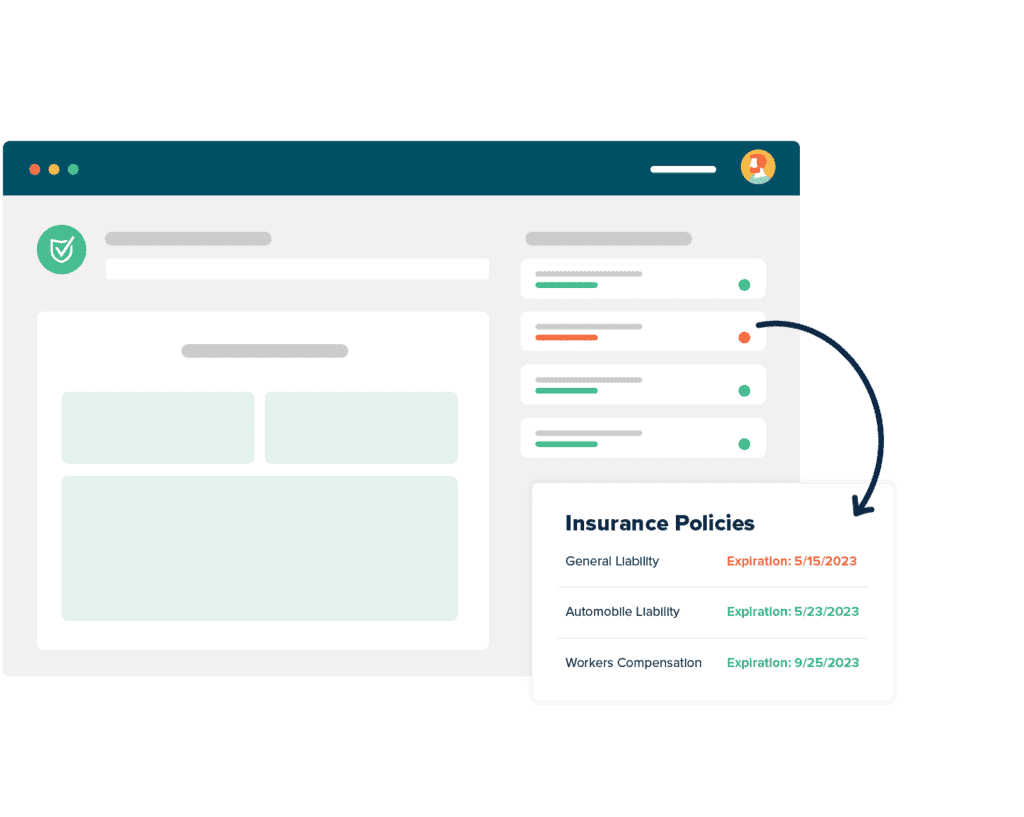

What Are The Benefits of COI Software?

What Our Customers Say

Adding Additional Insured To Certificate Of Insurance

Does your company work with a lot of vendors and contractors? Are you looking to hire subcontractors for an upcoming job? If so, you need to make sure your company is protected. That is why it is essential your vendors, contractors, and subcontractors have the right insurance coverage. You should ask them to produce a certificate of insurance, but you need to ensure you manage this appropriately. If you hire numerous contractors, each one of them is going to produce a certificate of insurance on your behalf. How are you going to keep track of this information? You have to use the right software program, which is where myCOI can help.

As you go through the documents in the tracking software, you will encounter language you need to interpret. For example, you may encounter COI additional insured. What is an additional insured? This means that you are covered by the insurance policy provided by the vendor. Even though the vendor protects themselves with this insurance policy, you may be included as an additional insured, meaning you have additional protection for losses a vendor causes. If you work with someone who provides you with insurance coverage as an additional insured, you can feel at ease, knowing you have the right level of protection.

You may be interested in adding an additional insured to the certificate of insurance. If you want to add additional insured coverage, you should talk with your legal counsel or your insurance agent or broker to determine what you need to do. That way, you can figure out what type of coverage you need, how much coverage you need, and how you want the coverage to be worded. Before the project starts, your business should ensure it has the right level of protection by examining the certificate of insurance.

Certificate of Insurance Additional Insured Sample

Before the project begins, you need to make sure your company is protected. One of the ways to do that is to review the certificate of insurance. Where can you find a certificate of insurance additional insured sample? A good place to look is at a certificate of insurance example PDF. The additional insured language on a certificate of insurance can be confusing; however, there are two common places you can look to find this type of language. You may find an arrow column in the middle of the form that says ADDL INSD. This column should be checked, and you should see the name of your company there, or there may be information related to the additional insured qualifications in the description of the policy at the bottom. You should see the company listed there as well.

When you review this information, you need to make sure it is accurate. For example, verify that your company name is spelled correctly if there is any information related to the effective date and the expiration date. Also, ensure the policy is still active and that you have the right level of coverage. All of this is important for making sure the company is protected before the project begins.

Certificate Holder Vs Additional Insured

Before you fill out the information for the project, make sure you understand the difference between a certificate holder vs. additional insured. In general, the certificate holder is the person who is receiving the COI from the insured. If you are the person receiving the certificate of insurance on behalf of the vendor, then you are the certificate holder.

For example, if you have a new project coming up, then you may need to know how to add a certificate holder to a COI. You may want to review a certificate holder insurance sample, so you understand how it is worded. Even though the company may have its own insurance policy, you may want additional coverage from the vendor as well. If so, the name of the company should show up in the additional insured section. This could be included as an additional insured on the policy, so take a close look at the certificate of insurance to see if it is listed.

Additional Insured Vs Named Insured

In addition, you may need to determine the difference between additional insured vs. named insured. In general, the first named insured is the party who purchases the insurance policy. Their name is usually listed on the policy declarations page. Then, there may be the option for the named insured to add additional insureds to the policy. That way, the additional insured has protection as well. In this case, you may be interested in additional insured coverage because you want coverage from the vendor’s insurance policy as well.

If you do want to be added to the insurance policy as an additional insured, your vendor may need to request this from their agent or broker to add an additional named insured endorsement form to the policy. If a contractor is hired to complete a job, they should carry an insurance policy they purchased for themselves. Then, the contractor may want to include the company that hired them as an additional insured on a policy. That way, the company is also protected against the work the contractors perform. Your risk management team is probably going to be responsible for reviewing the insurance. Then, if the company wants coverage, they will require coverage as an additional insured.

Who Should Be Listed As Additional Insured?

So, who should be listed as additional insured? It depends on how the project is unfolding, but if you would like this additional coverage for your company, then you should be listed as an additional insured on the insurance policies carried by your contractors. If you want to be added as an additional insured, you need to request that the vendor adds additional insured coverage to the policy by adding an endorsement form. Adding an additional insured to a policy does not have to be complicated, but you do have to request this in an agreement or contract.

If you are wondering if you already have coverage as additional insured, you can check your certificate of insurance copy. You may see a check in the box listed in a column in the middle of COI, corresponding with the policy this status applies to. This is one place where information related to additional insured status is listed. Or, you may see information related to additional insured status in the description box at the bottom of the page. Make sure you understand how much coverage your vendors have, the type of coverage your vendors have, and the limits of their coverage.

Why Request Additional Insured Status?

So, why request additional insured status? There are several reasons why this may be necessary. First, you never know if something is going to go wrong. If the subcontractor makes a mistake, you need to have the right type of protection. If something happens during the project, you may have to cover medical expenses, repair bills, and numerous other costs. This could be expensive, and you need to have insurance coverage under these circumstances. Even though the company may have its own insurance policy, the coverage may not be enough. You need to make sure the limit of the liability is high enough to cover potential repair costs and medical bills.

Make sure the additional insured contract language is appropriate. There is usually an additional insured clause, and you need to read this to make sure you have the right type of protection. If you file a claim, you need to feel confident it will be paid out. Otherwise, there is no point in getting this type of coverage. Make sure the additional insured clause will protect the company in the event of an accident. This is important as you examine the certificate of insurance.

Additional Insured Endorsement Forms

If you want to protect your company properly, you may need additional insured endorsement forms from your contractors. There are numerous types of additional insured endorsements, and you need your contractors to use the correct form to protect yourself and your company. You might be wondering, what is the purpose of an additional insured endorsement? Endorsement forms can help add new companies, like yours, to the insurance policy under the additional insured category. You need to ensure your company is included in the contractor’s insurance policy. That way, before the project begins, you will have the right level of protection.

When you work with a contractor, you probably expect the project to proceed smoothly. Even though there is a low chance of something going wrong, you still need to protect yourself in the event of an emergency. Something might break, or someone could get hurt. If that happens, your company needs to be protected. The only way you can do that is if you get your company added as an additional insured on the contractor’s insurance policy.

To get your company added, your contractor will need to communicate to their insurance agent or broker to add an endorsement form. There are plenty of endorsement forms available, and you need to know who is being added, what type of protection you have, and the limit of that protection. These endorsement forms can help you do that.