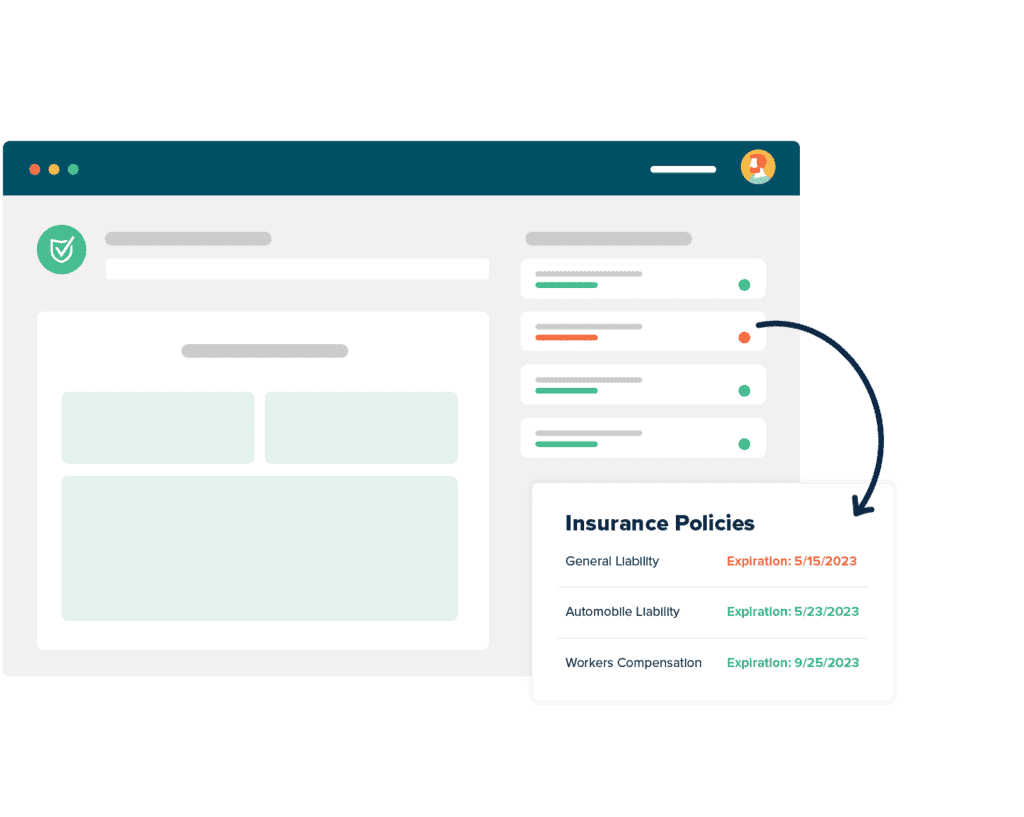

Best Certificate of Insurance Tracking Software

Automate Your COI Tracking

There’s no more need to worry about stacks of certificates cluttering up your office or hours of frustrating phone calls and emails to chase down certificates. myCOI Central provides your company with a solution to automate your insurance certificate requests, collection, and compliance resolution, while also giving your team a single, centralized repository to view compliance.

Protect Your Business From Costly Claims

Ask your CFO or Risk Manager just how much claims and lawsuits can cost your business. If you are collecting certificates just to confirm they were received, you have no guarantee that your requirements are being met. myCOI Central is built on a foundation of insurance industry logic to ensure you remain protected with the appropriate coverage.

For Agents & Brokers

Win business and boost retention by providing agency branded, industry leading insurance tracking software to your insureds. Offer software only or add on your own compliance review services.

What Are The Benefits of COI Software?

What Our Customers Say

Commercial General Liability Insurance

Commercial general liability insurance can be powerful protection against costly claims and lawsuits. If your company is just starting, you should seek the best general liability insurance for small business information to become better informed. Knowledge is power. The more you have, the easier it will be to find coverage that meets your particular general contractor insurance requirements. Additionally, you might be able to find cheap small business insurance that does not skimp on coverage.

The type and cost of general liability insurance small business owners should obtain matters. Their coverage must be sufficient at a reasonable price. They need to act intelligently when mitigating liabilities and planning for unfortunate events.

One thing to remember: you can be covered by any of the top 10 commercial insurance companies but what about your subcontractors? They should possess their own coverage so your company does not shoulder all of the liability risks that occur during the daily operation of your business. You should require the third parties your company hires to be covered and to prove their coverage by submitting certificates of insurance. These documents simply affirm the named insured, the subcontractor or vendor, is adequately covered.

You have to make sure your subcontractors submit valid and current certificates of insurance. One expired policy can spell ruin for your company if that particular third party injures someone. Your company could be on the hook for damages. Using an automated solution like myCOI can ensure every certificate of insurance you receive is up-to-date and meets your company’s requirements. You do not have to bear the entire weight of insurance tracking. You can save time and money when you use this cloud-based platform. You can tend to your other professional responsibilities more effectively when you do not have to worry about whether or not you are going to be sued.

General Liability Insurance Coverage For Small Business

General liability insurance coverage for small business is worth researching. The topic should be essential if you want to ensure your company’s future remains bright.

If you own your company or are your company’s risk management professional, then you should know the importance of protecting your organization’s assets from claims that emerge from normal business operations. Life is unpredictable. People make mistakes. Accidents happen. These statements are more than cliches. They are truths that should not be ignored.

Shopping for general liability insurance for LLC ventures takes time. Rushing into the process can result in expensive coverage that does not fulfill your needs. Discovering all the available options and then weighing them against your company’s needs should be a methodical process. You should want the best business liability insurance to protect your company. Small business insurance can make the difference between your company surviving a hefty lawsuit and going bankrupt.

If your company is a construction or contracting company, general liability insurance coverage for contractors should be required. If your company hires a handful of subcontractors, coverage should be mandatory. If your company hires hundreds of subcontractors, coverage should be mandatory. Transferring the burden of risk to them can place your company in a more comfortable position when it is not solely responsible for damages stemming from negligence. Lawsuits can ruin reputations and fortunes. What would happen to your company if an uninsured subcontractor you hired hurt someone while working for you? Could your company afford a huge payout?

Cheap general liability insurance for contractors can be found, but coverage must align with your company’s requirements. Your contractors should speak with an insurance agent or broker to get the best coverage at the best rate. Agents can guide contractors to what they need. A phone call or email can start the process.

Commercial General Liability Insurance Cost

Can your company afford a $1 million liability insurance cost? What about a $2 million liability insurance cost? A $5 million liability insurance cost?

How much does a $1 million dollar business insurance policy cost? How much is business liability insurance per month? How much is general liability insurance for an LLC?

If your company is new, what are its start up business insurance costs? What is the general liability insurance cost for contractors?

These are all great questions to research either online or by contacting an insurance agent or broker. Depending on your relationships with other companies, you can ask them for advice. Hopefully, they have seized the initiative and acquired coverage themselves. You can post questions on social media and other online forums if you can not find satisfactory answers. Some strangers would not think twice before helping others. You might find the information you need and possibly a new professional connection along the way. It does not hurt to ask. You can not receive answers if you do not ask questions. It also helps if you know what your company can afford.

Considering commercial general liability insurance rates is a wise practice. You want to keep your company protected from liability but you do not want your company going broke doing so. Paying high rates defeats the purpose of insurance if you can not afford them. Plus, sometimes the highest rates do not ensure the best coverage. The inverse can also be true: the lowest rates do not signify the worst terms. You have to put yourself out there to find suitable insurance at a price your company can afford.

The commercial general liability insurance cost should be factored into your company’s budget already. It should not be overlooked or avoided. You can think of it as just one more expense; the price of doing business.

General Liability Insurance Examples

What are some of the most common general liability claims? What does commercial general liability insurance cover? What does general liability cover for a business? What does general liability insurance cover for small business?

How much is general liability insurance for contractors? What is the best general liability insurance for contractors? Who provides general liability insurance for contractors near me?

Your questions about general liability insurance are as encompassing as the best comprehensive general liability insurance. Questions are good. Answers are even better. Both are worth seeking if you own a company. Information is crucial when shopping for insurance. Once you learn the details about insurance, you have to choose the issuer. General liability insurance examples can be effective testimonies to persuade you to choose one issuer over another. If an insurance company provides detailed answers and support, then what other superior services can they offer?

General liability insurance examples can be effective in learning what the insurance actually covers, what it does not cover, how much it costs, and more. Seeing insurance in use can show you some of the most common liability claims and what insurance plans cover them. Examples can also show you how much your company and contractors have to pay to remain covered. Examples can help you plan better. You might recognize certain illustrations mirroring your company’s situation. You could take that model and use it as a blueprint for finding the insurance that matches your company’s requirements.

The Internet is stocked with information. With vast volumes of data, it is important to not stick with one source. They can provide inaccurate or false information. You should use several sources to check the facts. Assuming you know the particulars of a policy can leave you underinsured and/or paying more than you should.

Professional Liability Insurance

What is the difference between professional liability insurance vs general liability? How is general liability insurance calculated for contractors? Is the professional liability insurance USAA provides worth investigating?

You can use professional liability insurance examples to help answer these and numerous other questions. Professional liability insurance can overwhelm those who do not know anything about insurance. Resources exist that can educate people about the subject.

Companies in various industries should be versed on the topic. Consulting agencies should have an inkling of knowledge about professional liability insurance for consultants. Medical organizations should be able to field questions regarding professional liability insurance for nurses. Contracting companies should know about professional liability insurance for individuals.

If you have researched several professional liability insurance companies, then you must come to a decision. What is the best professional liability insurance for your company?

Commercial general liability insurance is only one way to reduce liability risk. If your company hires subcontractors, then you should make them responsible for obtaining insurance. With this duty comes another one for your company: the collection and verification of certificates of insurance. Your company must do more than collect those documents. It must confirm that the coverage fits your company’s needs and is active. This is not a one-time action. Constant monitoring keeps coverage valid and current.

Although all of these tasks might seem time-consuming, myCOI can lend insurance expertise and automation to the entire process. Automating insurance tracking can simplify the workflows involved with the process as well as ensure stricter control over compliance practices. myCOI is powered by insurance experts who can provide your company with peerless compliance administration. You can trust the platform to help you and your subcontractors get it right when it comes to certificates of insurance.

Running a company amid a sea of risks can prove daunting. Fortunately, some aids can make every workday less stressful.