Best Certificate of Insurance Tracking Software

Protect Your Business From Costly Claims

Ask your CFO or Risk Manager just how much claims and lawsuits can cost your business. If you are collecting certificates just to confirm they were received, you have no guarantee that your requirements are being met. myCOI Central is built on a foundation of insurance industry logic to ensure you remain protected with the appropriate coverage.

Automate Your COI Tracking

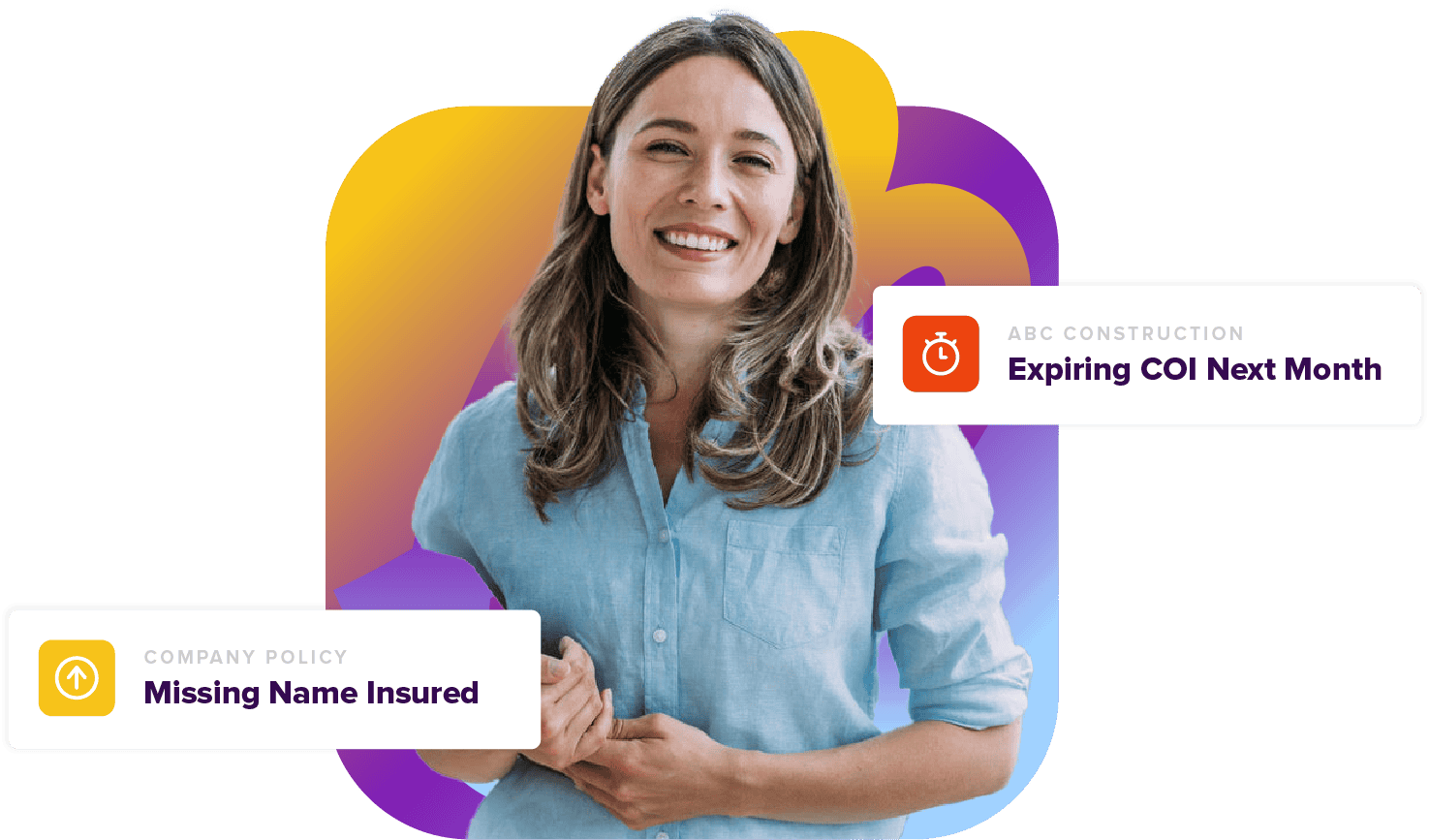

There’s no more need to worry about stacks of certificates cluttering up your office or hours of frustrating phone calls and emails to chase down certificates. myCOI Central provides your company with a solution to automate your insurance certificate requests, collection, and compliance resolution, while also giving your team a single, centralized repository to view compliance.

For Agents & Brokers

Win business and boost retention by providing agency branded, industry leading insurance tracking software to your insureds. Offer software only or add on your own compliance review services.

What Are The Benefits of COI Software?

What Our Customers Say

GC Certificate Of Insurance Tracking Platform

GC certificate of insurance tracking platforms (the GC stands for general contractor) are the tools large companies use to keep track of the hundreds of thousands of certificates of insurance they receive from general contractors. Each of those GCs needs to carry their own individual insurance protection, whether they’re a one-person company that insures only the sole proprietor, or a firm of dozens or hundreds of contractors. The risk generated by construction is not trivial, and it’s critical to the success of most construction companies that the subcontractors it hire assume the correct amount of risk.

A lot of young companies try to track insurance policies on Excel spreadsheets, and for a while that can work as an insurance tracking platform, but the sheer complexity being tracked on those certificates of insurance means that most companies outgrow Excel very quickly. That’s where solutions like myCOI come in, as a purpose-built certificate of insurance tracking platform.

At myCOI we offer the industry-leading certificate of insurance tracking solution, in a self-service SaaS solution as well as a concierge, managed service solution. We pioneered the COI tracking industry, you might say. And our team of insurance specialists, coupled with our commitment to customer service, makes us unmatched.

Anyone can download a certificate of insurance template and fill it in, make it look presentable, and deliver to a requestor. Yes, that’s dishonest and oftentimes illegal but it happens. Can your contracting business absorb the risk of not tracking for things like that? Or hiring full-time staff to hand-verify each one?

If you can’t, then a tracking solution may be a smart move.

Certificate Tracking

The competition in the certificate tracking space is fierce, and we’d be being dishonest if we didn’t say you need to choose the right solution for your company. Obviously, at myCOI we believe we are the right solution nine times out of ten, but we don’t fit every company, and that’s okay.

You’ll need to define what “success” means for your business. Is it the least expensive? That depends on how you measure cost. In pure dollars, a free COI tracking software may work, but is it reliable? Do its developers offer support? Are there regular product updates coming out? If not, check it carefully to make sure it isn’t out of date.

Is “best” the least of your precious person-hours consumed by tracking certificates of insurance? Then a managed solution like myCOI offers may be best. Our team of insurance professionals know what they’re looking at, and they’re experts in making sure your certificates are promising what they say they do, that they meet your business requirements for coverage, and our quarterly verification makes sure the coverage stays in effect.

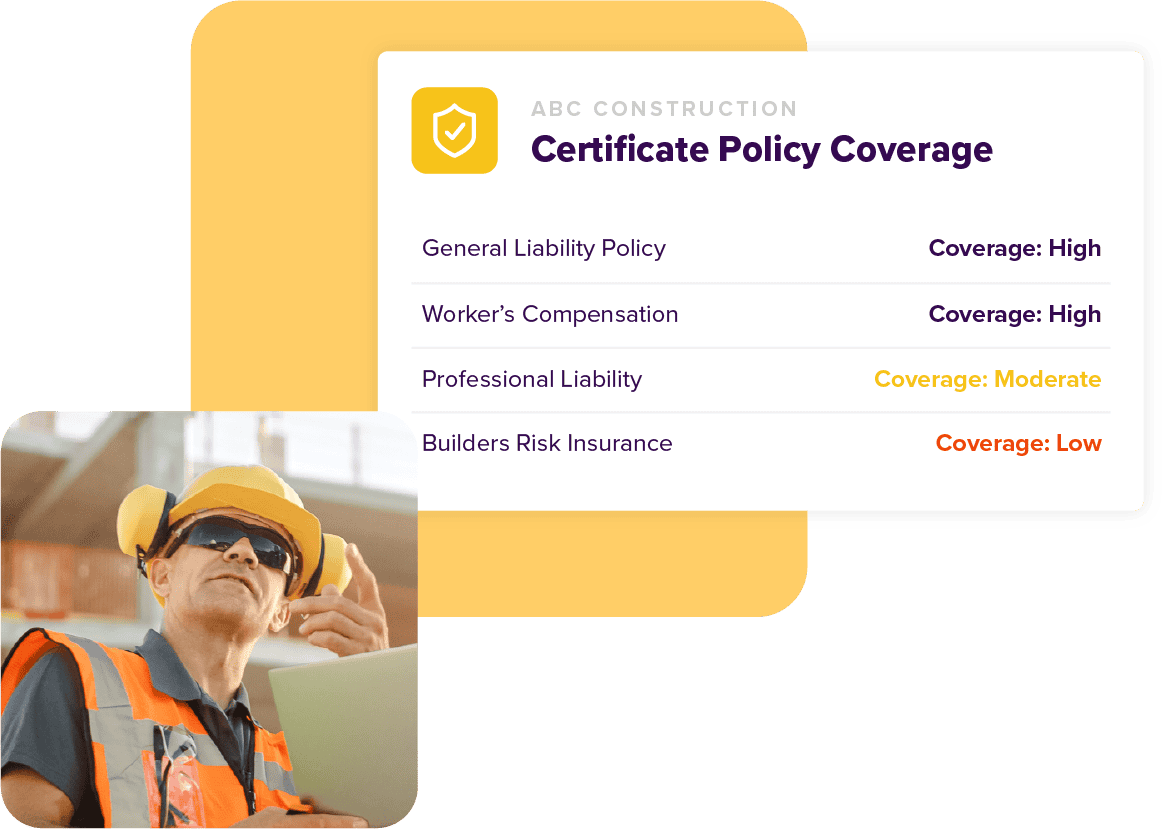

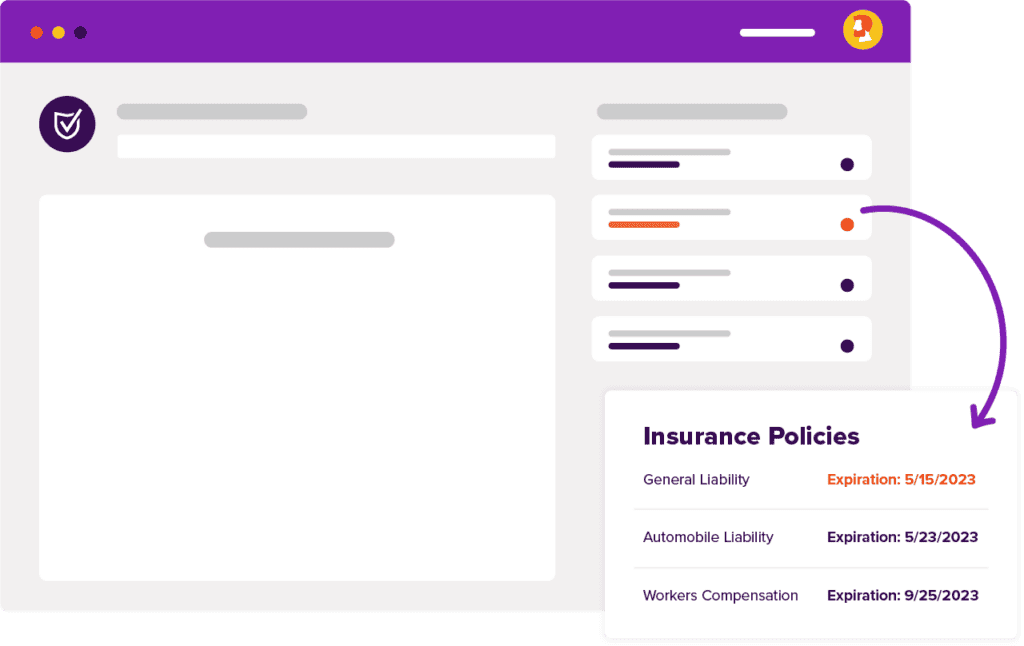

Take it from us, though, you need something more powerful than an expiration date tracker. Software to track expiration dates does nothing to confirm that the coverage on the COI matches the coverage you require, or that it’s even valid.

Free Renewal Tracking Software

Running a business is expensive, and sometimes the last thing you want to add is another expense, even when you have a need. We can’t tell you how many times we’ve heard companies tell us that they were doing their best: they knew about COI tracking software, but the budget was just too tight, so they did it with Excel or a free COI tracking software. Sometimes they tried to make do with free renewal tracking software or apps.

At a certain point, the amount of unnecessary risk they were assuming got to be too much, and they had to look for a more professional solution. Sometimes it’s because their risk management team or general counsel audits and realizes the exposure. Sometimes a new hire discovers a distressing reality that had gone unnoticed.

Unfortunately, sometimes it’s because the company just had to pay a damaging claim that they should have been covered for.

Free COI tracking software is not inherently bad, and almost no one sets out to make bad software. But it takes a dedication to customer service, a mission to erase worry, and a team of insurance professionals like the one we’ve assembled at myCOI to make sure your company is doing all it needs to with its certificates of insurance.

How To Organize Certificates Of Insurance

Knowing how to organize certificates of insurance for tracking is a necessity for any company that hires third parties such as contractors or vendors. A certificate of insurance tracking solution allows businesses to track certificate of insurance compliance

One of the most common mistakes that businesses make is not keeping accurate records of certificates of insurance. This puts them at risk for fines and penalties if they do not have up-to-date documentation on hand when requested by a third party, such as an attorney or law enforcement officer. In addition to having legal consequences, failing to keep track of your company’s certificates could lead to financial losses. It also increases the likelihood of liability lawsuits filed against your business. Knowing who needs to provide a certificate of insurance is one of the core components of risk management.

It’s not just those who hire contractors and vendors that need to track certificates of insurance. Property managers who host commercial tenants also need to ensure those tenants are carrying the proper insurance. We often see the duty of securing and verifying these COIs fall on property managers, instead of dedicated risk teams, so we strongly suggest having on hand a sample letter requesting certificate of insurance from commercial tenants, so you can quickly request the COIs you need to manage your property’s risk.

Certificate Of Insurance Tracking Template Excel

If you’re looking for a simple and manual way to track the certificates of insurance in your business, then using a COI tracking spreadsheet is an option worth considering. Many companies begin with solutions like having their staff track insurance policies on Excel spreadsheets. And for smaller companies just starting out, that system works. For basic certificate of insurance tracking spreadsheets are not a bad solution.

Many companies find spreadsheets a good training tool; for a certificate of insurance tracking template Excel has several basic templates that can be customized to what you need, but most companies scale past this very quickly.

The drawbacks of using an Excel insurance tracker are that they can be time-consuming to maintain and often require constant updating. What began as a simple project one person could track and easily snowball into a time-intensive process that’s impossible to scale as a company grows. Instead, companies might add more people and more spreadsheets, which leads to paperwork being lost or misplaced, which leads to increased chances for errors in the data.

That is exactly the worry that myCOI erases. Our systems are industry-leading. Our insurance professionals are top-notch. If you’re tracking hundreds or thousands of certificates of insurance, we’d love the chance to show you just how much time and effort we can save you.

It’s what we do.

How To Request A Certificate Of Insurance From A Vendor

In many cases knowing how to request a certificate of insurance from a vendor is either one of the simplest, or rarely the most time-consuming, part of a risk management team member’s job. In the former case, your company may have required a certificate of insurance for contractors who bid on the job, as part of the bidding process. Contractors need to know what their insurance costs will be to make a good bid, after all. It doesn’t do either party any good to bid on a job, win it, and then have to back out because you can’t afford additional insurance requirements.

In the latter case, when your company failed to request certificates beforehand, or worse, if you ask the project manager and they turn around and ask you “which vendors need a certificate of insurance?”, then you have more work to do. You’ll need to secure, or have secured on your behalf, certificates of insurance for each vendor or contractor.

How you do that depends on your business and the tools you use. In many cases you’ll just generate a letter requesting the certificate and send it to the vendor; in some cases, you may be requesting the certificate from the vendor’s agent or broker.

Many insurers and brokers have systems in place to receive these requests, and on your side, most teams maintain a sample letter requesting certificate of insurance from vendors, so you have a template to work from when necessary.

Certificates Of Insurance For Subcontractors

If you’re a subcontractor, or you hire subcontractors and have to track the certificates of insurance you receive from them, you may see a few oddities. Depending on what state you’re working in, certificates of insurance for subcontractors may sometimes lack evidence of workers’ compensation coverage. This is because several states do not require workers’ compensation coverage for what are called sole proprietorships, where the individual worker is the only employee of their one-person company. If you’re unsure whether or not there should be a workers comp policy by statute, consult with your state’s workers compensation board.

Even in states where it is not legally required, however, many companies that hire subcontractors still require the coverage as a necessity for employment. In that case, a workers’ compensation certificates of insurance for subcontractors will show the minimum necessary coverage required by the hiring entity.

What’s fun about these one-person plans is that often they’re what are called ghost policies: they are workers’ compensation plans, but they have exclusions disallowing coverage for the single employee. They allow subcontractors to satisfy the requirement of needing workers’ compensation, but since they are excluded, the coverage only covers a ghost.

Or in reality, no one.

If you need to request a certificate of insurance from a subcontractor, check with your risk management team. They may have a certificate of insurance request form template you can use. Alternatively, you can reach out to the subcontractor and remind them many insurance brokers and agents offer ways to request a certificate of insurance online.

Certificates Of Insurance Issues And Answers

We know this can be a complicated topic because we get asked about certificate of insurance issues and answers all the time. Insurance is a complicated field with nuances around every corner, and almost every situation has some kind of unique aspect. Understanding coverage, understanding what the certificates of insurance actually say—and what they don’t say—can be, and often is, a full-time job, and it often takes more than glancing at a certificate of insurance template.

There are two parties you want to check within almost any instance of questions around certificates of insurance. First, for questions like which vendors need a certificate of insurance, check with your company’s risk management department, or when that doesn’t exist, your company’s general counsel about what your vendor insurance requirements are. In many cases, these departments or people can give you a certificate of insurance review checklist to help you ensure that the COIs you review have all the necessary coverage.

The other party will be the agent or broker who issued the certificate of insurance. When you have questions about the coverage, exclusions, or limitations shown on a certificate of insurance you receive, the only safe source of information is the agent or broker itself. Don’t ask the third party who provided you with the certificate; not only does this give them the opportunity to be dishonest, it also sets you up to be taken advantage of out of ignorance or a mistaken belief about coverage. Go to the source. Ask the agent or broker. Certificate of insurance compliance is complicated enough without adding more chances for mistakes.