Best Certificate of Insurance Tracking Software

Automate Your COI Tracking

There’s no more need to worry about stacks of certificates cluttering up your office or hours of frustrating phone calls and emails to chase down certificates. myCOI Central provides your company with a solution to automate your insurance certificate requests, collection, and compliance resolution, while also giving your team a single, centralized repository to view compliance.

Protect Your Business From Costly Claims

Ask your CFO or Risk Manager just how much claims and lawsuits can cost your business. If you are collecting certificates just to confirm they were received, you have no guarantee that your requirements are being met. myCOI Central is built on a foundation of insurance industry logic to ensure you remain protected with the appropriate coverage.

For Agents & Brokers

Win business and boost retention by providing agency branded, industry leading insurance tracking software to your insureds. Offer software only or add on your own compliance review services.

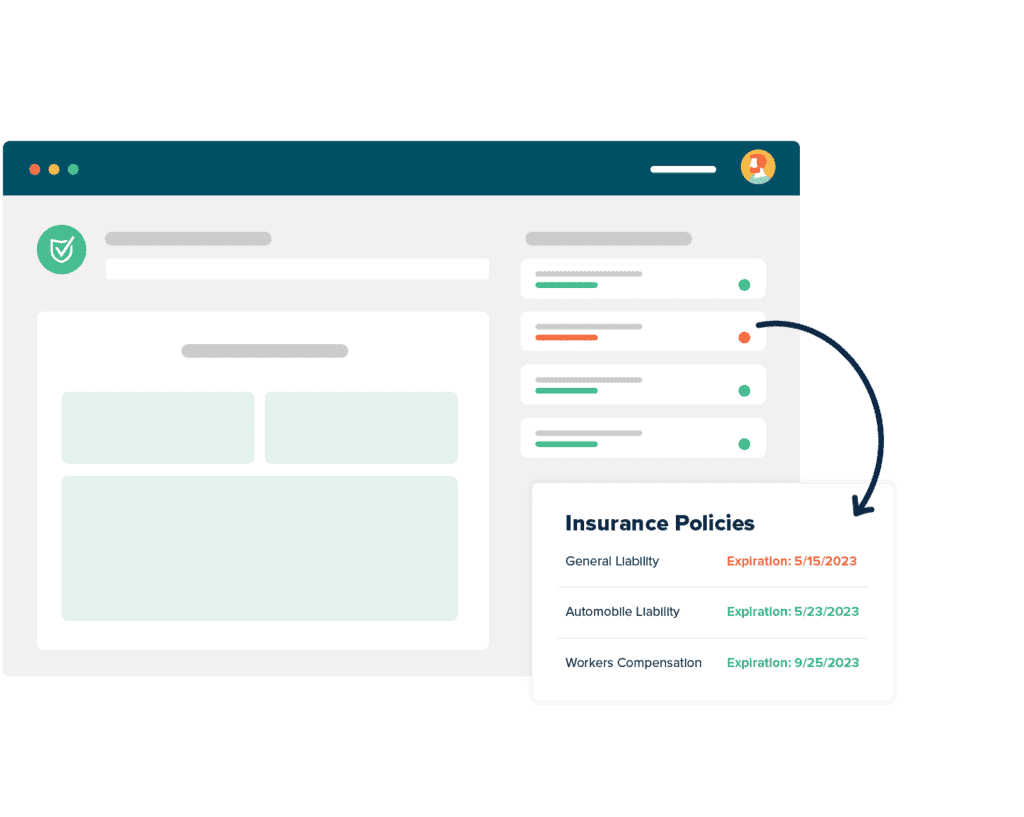

What Are The Benefits of COI Software?

What Our Customers Say

Liability Insurance Coverage

Operating a business involves more than hiring employees and marketing. If you own or manage a company, then you must also protect it in any way you can. You might have invested massive amounts of time and money into building something from nothing. You should not let your investments go to waste.

Anything that happens to your workers either through their actions or not becomes your responsibility. Whatever they do that does any damage to themselves, others, or property also becomes your responsibility. Liability insurance can protect your company and the third parties you hire from claims and lawsuits stemming from incidents.

Liability insurance provides a layer of protection that the most reasonable business plan can not. Insurance can both guard a company’s finances and give owners peace of mind. They can accomplish more when they do not have to worry about losing all they have created due to disastrous situations.

If you own a business, then you should choose appropriate liability insurance coverage. You should also make sure that your subcontractors own coverage. Certificates of insurance (COIs) prove people possess valid insurance. Understanding the intricacies of insurance can be daunting especially if you do not have the time. Knowing the ins and outs of COIs can overwhelm those who have to collect and manage them.

Insurance is not a topic to take lightly. Learning about liability insurance coverage is especially important if your company hires subcontractors. Partnering with a COI management solution like myCOI can help confirm they have suitable and sufficient coverage so your company is protected from costly litigation. Additionally, the weight of COI tracking can be lifted from you and your company, saving you time and money. You can tend to other responsibilities when you do not have to dwell on whether or not you are going to get sued. Liability insurance can make a world of difference.

Liability Insurance vs Full Coverage

What does liability insurance cover?

What does full coverage car insurance consist of?

Is comprehensive insurance full coverage?

The question of liability insurance vs full coverage typically arises when dealing with vehicle insurance. If your company works in the transportation or delivery industries, then you should learn the difference between the two concepts. Knowing what separates the two can make sure you and your subcontractors possess adequate coverage.

Auto Liability insurance only covers the cost of damages your third parties may cause to others while driving. Common damages are medical and vehicle repair costs.

Full coverage generally covers damages to others and their property as well as the damage to the vehicle that caused an incident.

Comprehensive insurance is not full coverage. Instead, it is one of two types of coverage that comprise full coverage. Comprehensive insurance covers non-collision-related events like vandalism, theft, and acts of nature. Collision insurance covers instances when collisions occur.

For example, if you cause an incident that damages another driver’s car and only own liability insurance, then their repair costs should be covered – not yours. If you own full coverage, then the repairs for both vehicles should be covered.

Liability insurance does not contain comprehensive and collision coverage. It might help you better to remember that liability coverage is separate from full coverage. They are two pieces of protection that when combined can guard against expensive claims.

Another major difference between the two is that many states require drivers to carry liability insurance whereas full coverage is not mandatory.

Depending on how comfortable you feel concerning your drivers’ risk, requiring both types of coverage can save your company financial headaches.

What if your company does not involve driving vehicles? What if it is a construction or contracting firm?

Then you should know that general liability insurance coverage is essential.

General Liability Insurance Coverage

Commercial general liability insurance is a powerful defense against claims and lawsuits, but it is not the only one.

A limited liability company (LLC) protects its owner from being responsible for liabilities. When an LLC is sued, the owner’s assets usually can not be targeted by plaintiffs. However, being an LLC is not the perfect alternative to being insured. General liability insurance for LLC adds more protection than what an LLC usually provides. An LLC can still be sued. General liability insurance coverage for small business is a topic worth researching. If you own your business, then one of your duties is to protect its assets from claims that emerge from regular business operations. This is where LLC insurance comes in. Life is unpredictable. So is running your company, regardless of its size.

If you own a construction or contracting company, then general liability insurance coverage for contractors should be mandatory. It does not matter if your company hires a few subcontractors or hundreds. People make mistakes. Accidents happen. Being covered is better than not owning any insurance. Lawsuits can cripple a company, forcing it into bankruptcy.

Can you rebound from such a defeat? Can you afford to pay damages out of your own pocket?

You can search for cheap general liability insurance for contractors online or you can contact your insurance agent or broker and ask them for quotes. Price is sometimes an indicator of quality. On the other hand, the most expensive coverage might not be the best fit for your situation. You should assess what you need before you query agents. If you do not know, then talk to agents anyway. They might guide you towards understanding your needs. You should also take your time learning the terms of a policy. Don’t settle for a policy because you’re in a rush. Informed decisions can protect your company better and keep your expenses to a manageable level.

Liability Insurance Coverage For Business

What does liability insurance cover for a business?

Liability insurance coverage for business, including professional liability insurance, guards against claims of negligence and injuries. It commonly offsets the costs of medical care, property repair or replacement, and legal fees.

Business liability insurance coverage is a kind of small business insurance that saves your company from having to reimburse people for alleged damages, injuries, or losses that stemmed from your employees during the normal course of operation.

General liability insurance coverage for contractors and general liability insurance coverage for small business basically share the same purpose: to shield your company from people requesting you pay them for supposed damages.

Construction and contracting companies have added risk simply because of the nature of their industry. Construction isn’t as safe as some people might think. Anything can go wrong on a job site. Equipment can malfunction. Severe weather can suddenly create dangerous environments. People can get hurt, even innocent bystanders. Construction material might fall from scaffolding. Errant machinery operators might back into someone’s car. No matter the cost, liability insurance can cover these events. Cheap general liability insurance for contractors is better than none.

General liability insurance for LLC may raise your company’s expenses. However, it is one charge that you should fit into your budget. Consider what you would have to pay out if you did not have insurance. Your company might close. Your personal assets could be wiped out. Your entrepreneurial spirit could be crushed all because you and your third parties were not insured.

Liability Insurance Example

What is general liability insurance coverage?

This is a question worth answering if you own a company. Once you acknowledge its importance, your next step should be to take action. Get covered. Require your contractors to own coverage and to prove it.

If you still do not see the point in liability coverage, finding a liability insurance example can be the tipping point. Personal liabilities examples can be effective testimonies. General liability insurance examples can be found online. Many insurance and financial websites offer definitions that explain the details of professional liability insurance and its ilk.

For instance, if your company sells products, then a product liability insurance example could demonstrate the importance of that particular type of insurance.

Liability insurance coverage is not an exciting subject to address. There are many nuances to consider, from terms to prices. Factor in the need for COIs and all they entail and insurance can become burdensome. Securing your company’s fortunes takes effort and money.

Would you rather pay this price of doing business or one that can shut your company down forever?

Earning profits is pointless if you do not take steps to preserve them. myCOI can lift some of the weight insurance can place on a company’s shoulders.

Obtaining, verifying, tracking, and storing COIs can be a rigorous task that calls for meticulous attention to detail and insurance knowledge. Companies that hire third parties must manage COIS for each contractor they hire. This total can grow out of control depending on a company’s success. It can rapidly overwhelm companies that are already busy or do not have enough staff.

myCOI is powered by insurance experts who can provide your company with peerless compliance management. Its straightforward usability and intelligent functionality make it a practical choice for businesses that want to reduce their risk.