Best Certificate of Insurance Tracking Software

Protect Your Business From Costly Claims

Ask your CFO or Risk Manager just how much claims and lawsuits can cost your business. If you are collecting certificates just to confirm they were received, you have no guarantee that your requirements are being met. myCOI Central is built on a foundation of insurance industry logic to ensure you remain protected with the appropriate coverage.

Automate Your COI Tracking

There’s no more need to worry about stacks of certificates cluttering up your office or hours of frustrating phone calls and emails to chase down certificates. myCOI Central provides your company with a solution to automate your insurance certificate requests, collection, and compliance resolution, while also giving your team a single, centralized repository to view compliance.

For Agents & Brokers

Win business and boost retention by providing agency branded, industry leading insurance tracking software to your insureds. Offer software only or add on your own compliance review services.

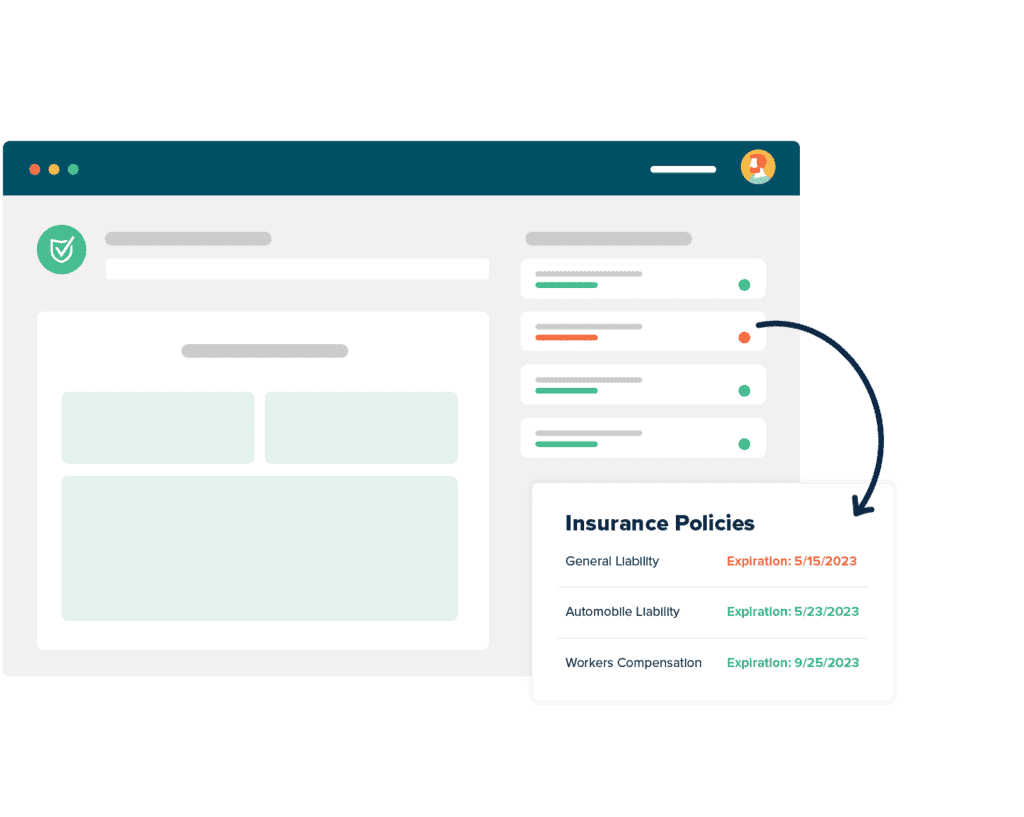

What Are The Benefits of COI Software?

What Our Customers Say

Certificate Of Liability Insurance PDF

So many of us, when we’re first starting out as risk management professionals or compliance administrators, start out looking at a certificate of liability insurance PDF. Sometimes it’s a blank one, like the ACORD 25 fillable PDF that we found by searching for a certificate of insurance online. Sometimes it’s a scary one, if we fall prey to a place that offers fake proof of insurance templates. In the end, though, we just put our heads down, run the checklist, and see what’s compliant and what’s not.

Pretty quickly though, we all get into the rhythm. Certificates come in and we depend on our processes to collect, track, and verify them against the requirements our company sets as a whole, plus any special considerations the specific job or project may dictate. If we have a good system, it’s a pretty manageable job.

Without a good system, it’s a nightmare.

At myCOI we erase your worry about certificate of insurance tracking. We offer both a self-service technology option you can use yourself, or a full-service managed service staffed with insurance industry experts with collectively decades of experience. Both of those options are there to let you focus on what’s important for your business, trusting that your risk is being managed the way you want it to be.

Sample Certificate Of Liability Insurance

Let’s take a moment and run through a sample certificate of liability insurance. In its most simple form, a certificate of insurance is the evidence from your insurer that you carry the insurance you claim to carry. The normal forms include all the necessary information a requestor would need to verify that you or your business carry the insurance they require of their contracted entities. Just like your driver’s license says your state believes you know how to drive safely, a certificate of insurance says your agent or broker believes you are covered. A certificate of insurance sample, even a certificate of insurance example PDF, will be useful guides.

There are nuances, of course. The certificate of insurance for businesses may be different, and will almost certainly carry different information, than the certificate of insurance for contractors, because the work done, the number of employees involved, and therefore the risk involved can be different.

A certificate of insurance also removes the need for unnecessary conversations. If you’re being considered for a job, competing on the bid is enough work. Not having to explain your insurance coverage, because your certificate of insurance explained it for you, can be a real time saver.

Remember too that insurance requirements vary by state, which means that certificate of insurance requirements by state vary also. Knowing when to request a certificate of insurance or, if you’re on the receiving end, how to check certificates of insurance can often be the difference between risk being managed and risk being out of control. A certificate of liability insurance is that powerful.

Certificate Of Insurance

The concept of a certificate of insurance is not a new one. In a very basic form, you probably have a certificate of your auto insurance in your car or your wallet. The form is a bit more complex for business general liability insurance, but the concept is the same: a document issued by an insurer saying that the bearer is insured against certain actions to certain levels of protection. The most common certificate of insurance template is the sample ACORD 25.

Most agents or brokers will give you a certificate automatically, or offer you a way to request your certificate of insurance online via their website.

Now that we’ve talked about how important certificates of insurance are, let’s look at a certificate of insurance explained. By far the most common general liability form is the ACORD 25 general liability insurance form.

All of the fields are clearly labeled, and your agent or broker should provide it to you already filled out, but let’s look at the high points. The Insured box should have your name or your company’s name in it since it’s certifying your insurance. Depending on your coverage, you may see values in the General Liability box, the Automobile Liability box, or the Umbrella/Excess Liability box, and so on.

Certificate Of Insurance For Business

When it comes to needing a certificate of insurance for business purposes, much depends on which business you are in that relationship. Let’s first look at when you’re the requesting business: you’re hiring contractors or vendors and you need to ensure they’re carrying the requisite coverage to shield your company from risk they create, without exclusions or limitations that your business won’t accept.

It almost goes without saying that you’re also on the lookout for fake business insurance templates or other attempts at fraud.

In this instance, you probably have either a tool like myCOI to help you with this, or you have a risk management checklist of some sort to check the certificates of insurance against. One common check is to decide whether your company needs to be just the insurance certificate holder vs additional insured; being endorsed as additional insured can extend coverage to your organization in the event of a loss or litigation caused by the third party you hire.

And if you’re on the other side, the contractor or vendor providing the certificate of insurance, all you really need to do is consult with your broker or other insurer, ensure you meet and can accept all the coverage requirements requested, and get an acceptable certificate of insurance issued by your broker.

How To Request A Certificate Of Insurance From A Vendor

In many cases knowing how to request a certificate of insurance from a vendor is either one of the simplest, or rarely the most time-consuming, part of a risk management team member’s job. In the former case, your company may have required a certificate of insurance for contractors who bid on the job, as part of the bidding process. Contractors need to know what their insurance costs will be to make a good bid, after all. It doesn’t do either party any good to bid on a job, win it, and then have to back out because you can’t afford additional insurance requirements.

In the latter case, when your company failed to request certificates beforehand, or worse, if you ask the project manager and they turn around and ask you “what is a certificate of insurance for vendors?”, then you have more work to do. You’ll need to secure, or have secured on your behalf, certificates of insurance for each vendor or contractor.

How you do that depends on your business and the tools you use. In many cases you’ll just generate a letter requesting the certificate and send it to the vendor; in some cases, you may be requesting the certificate from the vendor’s agent or broker.

Many insurers and brokers have systems in place to receive these requests.

Proof Of Business Insurance Template

You’re a contractor, a subcontractor, or other vendor who does business with other companies. You’re looking at setting up a new client relationship. And at one point, you’re going to hear “great, we just need proof of business insurance for our records.” You’re going to hear that a lot. So it pays to be ready for it.

Proof of business insurance most often means a certificate of insurance, and for new contractors, that can be a new and scary thing. But looking at a proof of business insurance template, like an ACORD 25 example, will help you realize it’s a lot less intimidating than it seems. Plus, the best and safest way to get one is to request it from your insurance broker, not fill it out yourself.

What you should focus on, though, is checking that what the certificate says is what the client you’re trying to win requires. Each company, and each state, has their own requirements when it comes to insurance, so you may want to double-check what your broker provides to make sure you’re carrying the coverage required. Look again at that ACORD certificate of insurance sample and make sure you recognize what each box is talking about.

Sample Certificate Of Insurance With Additional Insured

IRMI—the International Risk Management Institute—defines an additional insured as “a person or organization not automatically included as an insured under an insurance policy who is included or added as an insured under the policy at the request of the named insured.” That translates quite often as “I need to extend the coverage I purchase from my insurer to the third-party hiring me to do some work.”

A sample of additional insured endorsements is relatively easy to find online. A quick search will turn up a plethora of certificate of insurance additional insured wording. What you’re going to see is a standard certificate of insurance, but with the addition of the additional insured. Be careful that you don’t mistake a sample certificate of insurance with additional insured for an example of the kind of coverage you need to secure for your business; that’s a conversation you need to have with your insurer, not something you get from a PDF. A sample COI with additional insured is just meant to be an example of format.

Blanket Additional Insured Wording On Certificate Of Insurance

Investopedia defines blanket additional insured wording on certificate of insurance as “an insurance policy endorsement that automatically provides coverage to any party to which the named insured is contractually required to provide coverage. A blanket additional insured endorsement is most commonly found in liability insurance policies, though it is typically not a feature of the policy language.” Quite often, people choose blanket endorsements because they work with so many companies that securing individual endorsements is too time and effort-consuming to be practical.

Like a named additional insured endorsement, a blanket additional insured endorsement extends the insured’s policy protection to another party. However, many insurers stipulate additional requirements for entities to qualify for blanket endorsement, the most common of which is that the two parties have a business contract in place. Check your business’ sample additional insured wording; it can often guide you in the right direction.

Deciding whether your business can accept a blanket endorsement vs specific endorsements is a question for your counsel or your risk management group. There are pros and cons to each, and in many cases certificate holders often stipulate that a specific endorsement is required, so that there’s no danger of claim denial.