Best Certificate of Insurance Tracking Software

Protect Your Business From Costly Claims

Ask your CFO or Risk Manager just how much claims and lawsuits can cost your business. If you are collecting certificates just to confirm they were received, you have no guarantee that your requirements are being met. myCOI Central is built on a foundation of insurance industry logic to ensure you remain protected with the appropriate coverage.

Automate Your COI Tracking

There’s no more need to worry about stacks of certificates cluttering up your office or hours of frustrating phone calls and emails to chase down certificates. myCOI Central provides your company with a solution to automate your insurance certificate requests, collection, and compliance resolution, while also giving your team a single, centralized repository to view compliance.

For Agents & Brokers

Win business and boost retention by providing agency branded, industry leading insurance tracking software to your insureds. Offer software only or add on your own compliance review services.

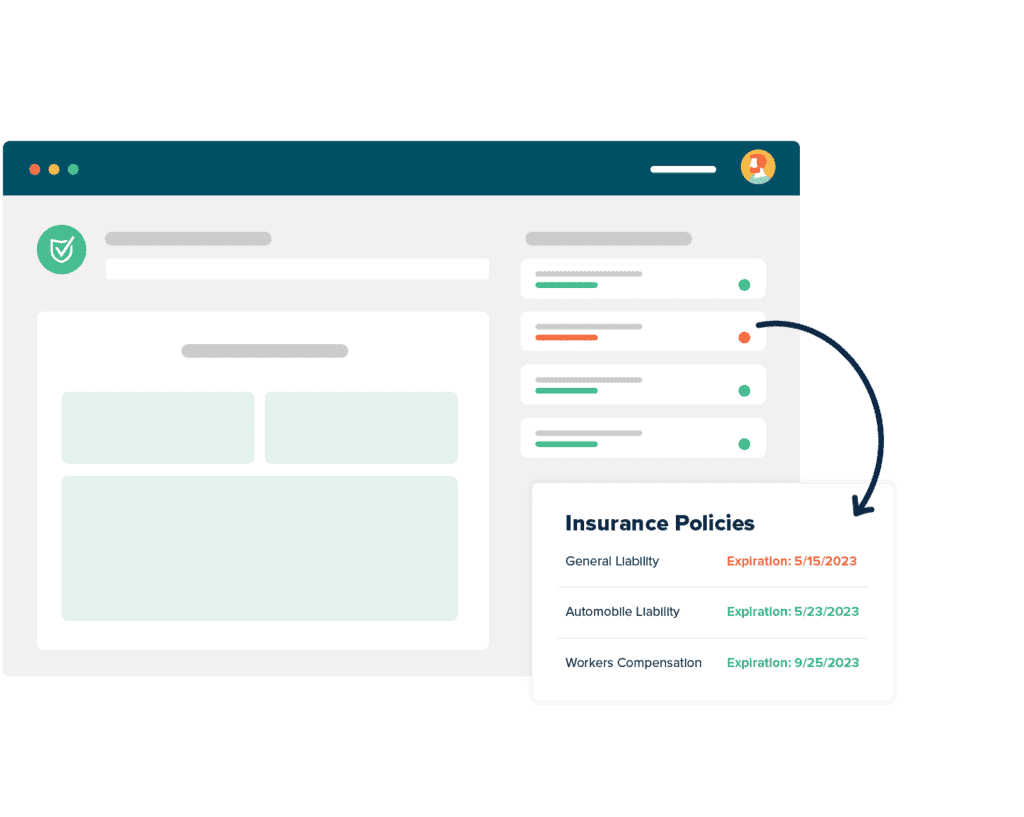

What Are The Benefits of COI Software?

What Our Customers Say

Personal Certificate Of Liability Insurance

At myCOI we get a lot of questions usually questions around a certificate of insurance. Sometimes it’s simple things like “where can I get a personal certificate of liability insurance?” or “can you tell me about cheap general liability insurance for contractors.” Sometimes the questions are more specialized, because we have one of the best teams of insurance experts around. We do our best to answer them, or to refer the questioners to the correct people to answer those questions, if it’s not us. That’s just who we are.

Certificates of liability insurance are one of the most common pieces of insurance paperwork in use. Across the United States, tens of thousands are requested, delivered, or reviewed every working day. These certificates are essentially certifications: strictly streaking, certifications from the agent or broker that the named insured carries the coverage the certificate states at the time the certificate was issued. In a more general sense, promises from one company to another that they can trust each other to do business.

There are almost no businesses that won’t have to deal with a certificate of liability insurance at least once during the course of business. Knowing how to accurately request, receive, verify, and track certificates is often specialist knowledge that teams don’t try to learn before it’s later than it should be. But we’re here to help.

Let’s get started.

Certificate Of Liability Insurance Template

You’re a contractor, a subcontractor, or another vendor who does business with other companies. You’re looking at setting up a new client relationship. And at one point, you’re going to hear “great, we just need proof of business insurance for our records.” You’re going to hear that a lot. So it pays to be ready for it.

Proof of business insurance most often means a certificate of liability insurance insurance form, and for new contractors, that can be a new and scary thing. But looking at a certificate of liability insurance template, like an ACORD 25 example, will help you realize it’s a lot less intimidating than it seems. Plus, the best and safest way to get one is to request it from your insurance broker, not fill it out yourself. Just because you find a certificate of liability insurance form example doesn’t mean you should use it, and when you need an insurance certificate template Word is the worst choice.

What you should focus on, though, is checking that what the certificate says is what the client you’re trying to win requires. Each company, and each state, has its own requirements when it comes to insurance, so you may want to double-check what your broker provides to make sure you’re carrying the coverage required. Look again at that ACORD certificate of insurance sample and make sure you recognize what each box is talking about.

Do not fall prey to the temptation of doing this yourself. A certificate should be issued by your agent or broker. Just because you can go to the internet and download a certificate of liability insurance form PDF fillable by anyone with a computer, doesn’t mean you should. You shouldn’t. This is a legal document. It needs to be filled out by a professional capable of certifying what it says, not by you and your best guess.

ACORD Certificate Of Insurance Sample

It may be helpful to take a look at an ACORD certificate of insurance sample. You’ll want to start with an ACORD certificate of liability insurance PDF certificate example, the ACORD 25. It is the most commonly used general liability certificate template.

There are a lot of boxes out on this form. Whether you’re reviewing a certificate issued by your agent or other insurer, these include:

- You need to make sure your general liability insurance is listed. This typically includes the per occurrence limit and the aggregate limits of the policy.

- You also need to confirm the policy number. This includes the policy effective date and the policy expiration date.

- If you have automobile liability insurance, you need to include this as well. Again, make sure you confirmed the policy number, effective date, and expiration date.

- If you have workers’ compensation and employers t liability insurance, you should include all of this information as well. This includes the policy number, effective date, and expiration date.

- You may also have an umbrella or excess insurance policy. An umbrella or excess policy is a policy that kicks in if you exceed the maximum liability on some or all of the underlying insurance policies.

If you have questions about how an ACORD form should be filled out properly, you may want to take a look at an ACORD form sample for help. Like most things, as a year for searching for things like ACORD certificate of liability insurance 2020 was a good one; a quick Google search will turn up what you need, no problem.

How To Get A Certificate Of Liability Insurance

Answering the question of how to get a certificate of liability insurance depends entirely on who you are and what your role is in the certificate of insurance process, because it affects both sourcing and propriety.

Let’s imagine first that you’re a contractor, vendor, or other third-party who is being asked to provide a certificate of insurance before you can begin work. In this case, you want to start with your insurance agent or broker’s website. Many providers offer forms that allow you to request the correct certificate without having to make an appointment or make a phone call.

What you should not do, though, is start wondering how to get a certificate of insurance online yourself, so you can fill them out without your agent. Don’t do that. Never do that. Let your insurance agent or broker do that. It’s their job, they’re the experts.

If you’re a certificate holder (the person or entity who receives certificates of insurance) and you need to request updated certificates, you can also start at the insurer’s website, if you know which agent to check out. This can happen in some instances when a certificate holder needs a new or updated certificate because of discrepancies or questions.

Lastly, if you’re an insurer looking for form templates, or even sitting at your computer asking “how do I fill out an ACORD certificate of insurance,” check with your senior leadership or check online for resources. ACORD provides helpful instructions for agents and brokers about filling out their forms.

Certificate Of Liability Insurance Cost

Certificate of liability insurance cost usually comes up with a question like “how much does the certificate cost?” The short answer to that is it shouldn’t cost anything: most agents and brokers provide them at no charge and assume the cost out of the premiums you pay. It’s in everyone’s best interest for the insurance coverage you purchase to be clearly understood by all parties: the last thing anyone wants is to be held responsible for a claim because of something simple like the cost of a certificate.

We like to think about certificate cost from another point of view, however. We take the point of view of the certificate holder, the entity that will be receiving the certificate of insurance, and the idea of the cost of not securing and tracking certificates of liability insurance. Not insisting on and then verifying certificates can cost a company quite literally everything.

It costs money to maintain insurance, yes. And it costs money to require certificates of insurance, to insist that every contractor, vendor, or other third-party provide them. It costs money to verify the coverage details, to follow up and ensure the coverage doesn’t lapse, to confirm that when insurance requirements change that the vendors adapt their coverage. It’s often not an insignificant cost, either.

But the cost of failing to do it is potentially so much higher. Can you really afford not to do it?

Certificate Of Insurance For Small Business

The needs for a certificate of insurance for small business operators are the same as any other business. If your small business is hiring contractors, you will want to collect and verify a certificate of insurance for contractors you hire. Any contractor who will be working in or around your business premises should be providing you with proof that they carry the coverage you demand of them to ensure you’re not assuming liability for risk that they cause. It doesn’t really matter whether you have the best general liability insurance for small business: if you accept responsibility for risk you shouldn’t, it could cost you.

Sometimes small business owners consider not securing certificates of insurance because they’re concerned about costs, but this isn’t a valid concern. Any certificate of insurance cost is borne by the insured, but that cost should be zero. There have been some cases of insurers requiring fees to replace certificates of insurance, but almost every agent or broker will provide these at no cost.

On the other end of the spectrum, if you’re a small business owner wondering how you gain certificates of insurance for your own small business insurance, the process is the same. Speak to your agent or broker or see if you can request the necessary certificates online from their website. When it comes to liability insurance small businesses have just as much need as any other business.

Small Business Insurance Cost Calculator

myCOI is not an insurer, so we’re not going to offer you a small business insurance calculator that will, for example, allow you to enter X amount of coverage over Y amount of assets and get back Z, an estimated premium. That’s not our business. There are plenty of businesses that do that.

What we will talk about, instead, is the advisability of maintaining stable insurance coverage. We hear stories, sometimes, about businesses that look for very short-term policies. They want to know how to get a certificate of liability insurance for an event, right before the event. Many people sell short-term insurance, and if the work is far outside your normal zone of coverage, that may be a good solution. But don’t discount the first, the cost savings associated with a longer-term policy, and second, the benefits of a more stable relationship with your agent or broker.

The next time you feel the urge to Google “how to get a certificate of insurance for an event,” stop and think first. Consider changing your search to “how much does general liability insurance cost for a sole proprietor?” (if you are a sole proprietor, otherwise change it to ‘small business.’ Balance the short-term cost against the long-term cost. What if you need this coverage six times this year? Is the short-time cost still worth it?

Every dollar is precious when you’re a small or young business. Be a good steward of your money and do your due diligence.