Best Certificate of Insurance Tracking Software

Automate Your COI Tracking

There’s no more need to worry about stacks of certificates cluttering up your office or hours of frustrating phone calls and emails to chase down certificates. myCOI Central provides your company with a solution to automate your insurance certificate requests, collection, and compliance resolution, while also giving your team a single, centralized repository to view compliance.

Protect Your Business From Costly Claims

Ask your CFO or Risk Manager just how much claims and lawsuits can cost your company. If you are collecting certificates just to confirm they were received, you have no guarantee that your requirements are being met. myCOI Central is built on a foundation of insurance industry logic to ensure you remain protected with the appropriate coverage.

For Agents & Brokers

Win business and boost retention by providing agency branded, industry leading insurance tracking software to your insureds. Offer software only or add on your own compliance review services.

What Are The Benefits of COI Software?

What Our Customers Say

What Is A Certificate Holder On Insurance

There are a lot of labels on a certificate of insurance form, and if you’re not familiar with them, they might sound a little weird. For example, one field is labeled “certificate holder.” The certificate holder is the party the certificate of insurance is provided to. So if you’re hiring someone, and you requested the COI, then you’re the certificate holder.

If that’s not clear enough, a simple internet search for “certificate holder insurance sample” will show you plenty of examples so you can parse it out for yourself.

Certificate Holder Vs Insured

Knowing who should be listed as certificate holder on a certificate of insurance is a key piece of certificate tracking knowledge. In almost every case, the certificate holder is the employing entity. Let’s look at a quick example.

Your general contracting company is working on a new building. You subcontract out the drywall installation and, as a matter of course, request a certificate of insurance from the drywall subcontractor. Your general contracting company becomes the certificate holder, because you’re holding the COI that you received.

Now, remember, there are clear demarcations between the insurance certificate holder vs policyholder. The drywall subcontractor is the policyholder, not your company. And, because this is where insurance gets complicated, there could be a difference between you as the certificate holder vs an additional insured, when it comes time to adjudicate any claims or losses.

This complexity is why it is critical to have a trained insurance professional setting your company’s insurance guidelines, and just as critical that your risk team is tracking and verifying the certificates of insurance for business as they come in.

How To Request A Certificate Of Insurance From A Vendor

If you’re a contractor or company asking “when do you need a certificate of insurance from a vendor?” The answer is pretty simple: before any vendor that enters your company premises or project site to perform work and takes any actions that may generate any risk at all needs to give you a certificate of insurance.

That sounds pretty vague, we know, but it’s a simple reality. Risk exists all around us, whether we generate it or not, and the last thing you want to do is assume the burden of risk your vendor opened you to because you failed to secure a certificate of insurance.

Now you may ask “what is a certificate of insurance for vendors?” and the answer is, the same thing you provide to other entities that you do work on behalf of. It should show the vendor’s coverages,, and all the usual information. You should request certificates of insurance from vendors every time you hire them.

Knowing how to request a certificate of insurance from a vendor likely comes down to how your company works with vendors. In many cases, COIs with the minimum insurance requirements for vendors are required as part of the vendor application process or were specified in the RFP, or in an agreement or contract. If not, it’s often a requirement before the vendor can begin working.

If you deal with a lot of vendors, you can often save a lot of time by having a request for certificate of insurance sample letter on hand. Knowing how to request a certificate of insurance from a vendor does little to shield you from the hours of work you have ahead of you verifying all those resultant COIs, though.

Certificate Holder Vs Additional Insured

This distinction is perhaps one of the most important in the insurance industry when it comes to certificates of insurance and additional insureds: the relationship between the insurance certificate holder vs additional insured. And that most often happens because people don’t understand what it means to be a certificate holder. At myCOI we get asked “is certificate holder the same as additional insured?” all the time.

A certificate holder, put baldly, is the person or organization that holds the certificate. If you receive a certificate of insurance from a hired third party, you’re the certificate holder. That doesn’t automatically mean that you receive additional insured protections; that can only happen if the certificate carries a scheduled or blanket additional insured endorsement to the policy, and your company meets the requirements of the insurer to receive this coverage.

One of the most common mistakes we correct at myCOI is certificates that lack the additional insured information that the certificate holder requires. Simply holding the certificate does not offer you the protection you require, and verifying that status is a key component of our service and technology.

Remember, claims often come down to determining who has the final assumption of the liability for the action that caused the claim. When it comes down to certificate holder vs additional insured, or even policyholder vs certificate holder, the decision will come down to what’s in the policy, and what assertions were made at the beginning of the relationship.

Certificate Of Insurance Explained

If you’re a contractor, you need to have a certificate of insurance for the insurance policies your company has. There are probably lots of insurance policies you carry at your company. These include:

- General liability insurance, which covers the potential liability you take on with each project, such as construction projects

- Commercial auto insurance, which covers your vehicles and drivers during the job

- Commercial property insurance, which protects any real estate you might have or lease for your company

- Workers compensation and Employers Liability

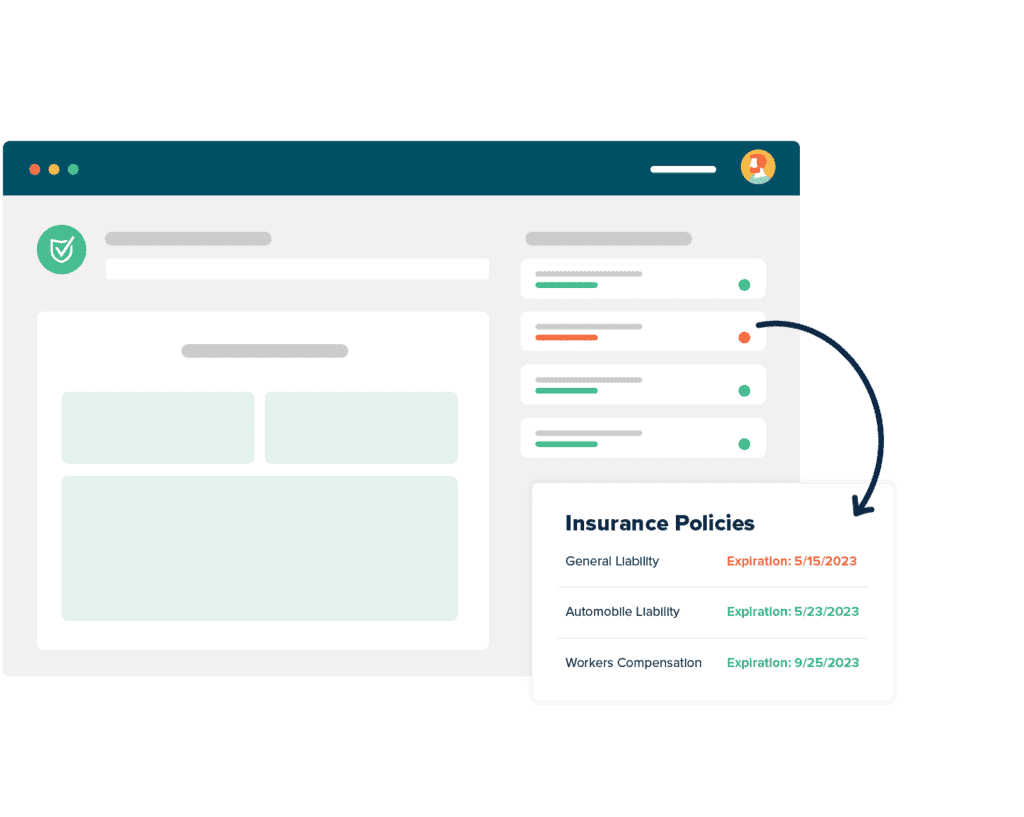

When it comes to certificates of insurance 101, you need to make sure you have accurate certificates to represent all of your policies. Don’t just trust a certificate of insurance PDF. Know what you’re looking for. A few critical elements include:

- The limits of your protection

- The effective and expiration dates, which define when that policy is active

- Your insurers or carriers, which are your insurance companies

You should not be creating your own COIs. Even though you should review your certificates, it is essential to rely on a specialized third party like your insurance agent to produce them. This is one of the services that your policy premiums pay for. That way, you know you have the proper protection for your company the next time you start a project.

And remember that certificate of insurance requirements by state can be very different. Let’s imagine you’re headquartered in Cincinnati, which puts you in working distance of both Indiana and Kentucky. All three of those states could have differing regulatory requirements around insurance and compliance, and it’s your responsibility to be compliant.

Sample COI With Additional Insured

A simple search online will show you plenty of additional insured examples, with enough variety that you can find an example for all types of certificate of insurance endorsements. Additional insured endorsement forms take a common shape: most include a warning right at the top that says “this endorsement changes the policy; please read it carefully.” This is an important distinction because, as we’ve already discussed, you’re amending your prior coverage to additional coverage for the entity named.

Next on an additional insured endorsement example, you may see “Additional Insured – Names Person or Organization.” This may seem like just a field label, but it carries the weight of precedent. It’s not unheard of for a claim to be adjudicated against a putative additional insured because they didn’t take the time to check their additional insured endorsement forms to make sure their name was spelled correctly.

Most additional insured endorsements forms will also have a short section noting that this endorsement modifies the “who is an insured” definition from the original certificate of insurance. It may seem unimportant, but on a certificate of insurance additional insured wording can often be critical.

If this doesn’t make sense, take the time to look up a certificate of insurance additional insured sample that is applicable for your industry and your state. Quite often, just seeing what a sample additional insured endorsement looks like is enough to help it begin to make sense.

Certificate Of Insurance Sample PDF

If you’re a contractor or a vendor, an ACORD certificate of insurance sample is only one of the many types of insurance forms you might be looking at every day.

At its most basic, this certificate has all the relevant information regarding your insurance policy. There is a lot of information that could be included on this form. For example, this form might have information on when the policy comes into play, its duration, who owns the policy, what the limit on the policy is, and who you need to contact if you need to file a claim.

If you are looking for a sample certificate of insurance with additional insured, though, then you might be looking for a slightly different document. This certificate includes added endorsements in very specific situations. If you need a certificate of insurance with additional insured, you need to reach out to the insurance agent or broker to make sure you have this type of coverage.

If you’re looking for a certificate holder insurance form, well, stop looking. That’s not a thing. A certificate holder is an entity that receives the certificate of insurance from a contractor, vendor, or another provider. If you receive certificates, that’s you. If you provide them to companies that hire you, that’s the company hiring you.

Remember that a certificate of insurance sample is just that: a sample. Not an example, and certainly not proof of coverage.