Best Certificate of Insurance Tracking Software

Protect Your Business From Costly Claims

Ask your CFO or Risk Manager just how much claims and lawsuits can cost your business. If you are collecting certificates just to confirm they were received, you have no guarantee that your requirements are being met. myCOI Central is built on a foundation of insurance industry logic to ensure you remain protected with the appropriate coverage.

Automate Your COI Tracking

There’s no more need to worry about stacks of certificates cluttering up your office or hours of frustrating phone calls and emails to chase down certificates. myCOI Central provides your company with a solution to automate your insurance certificate requests, collection, and compliance resolution, while also giving your team a single, centralized repository to view compliance.

For Agents & Brokers

Win business and boost retention by providing agency branded, industry leading insurance tracking software to your insureds. Offer software only or add on your own compliance review services.

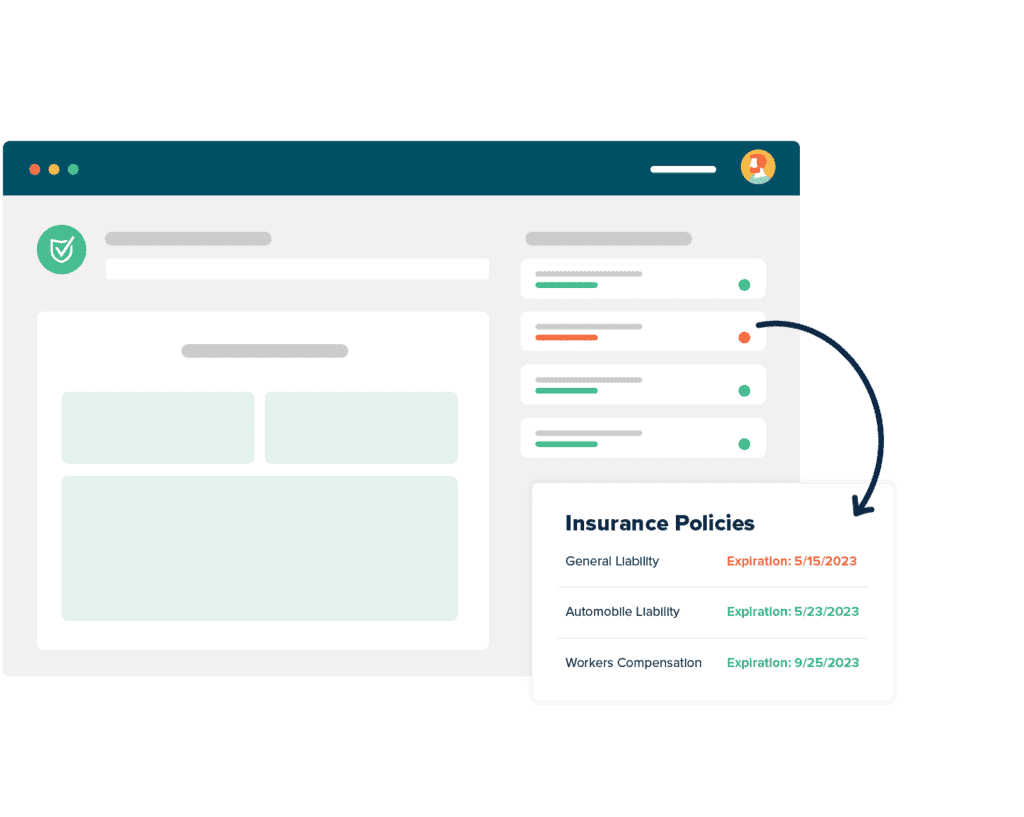

What Are The Benefits of COI Software?

What Our Customers Say

Construction Liability Insurance

Construction liability insurance, sometimes called contractor’s insurance, is the protection contractors buy to protect their businesses from property damage, injuries, and accidents. Put another way, It is one type of insurance for construction company protection. Construction and contracting are industries rife with the opportunity for risk. Consider: workers with power tools, on the ground or on ladders and scaffolding, with varying levels of experience and skill, often outside exposed to whatever the weather is that day… and that doesn’t even take into consideration whether or not they’re doing the work correctly.

Or if they’re using the right materials. Or working from the correct plans. Or doing the work at the right address. Or in the proper order of operations.

These are the questions that keep construction insurance types awake at night. All of them are unlikely, but that’s the definition of an accident: something you didn’t expect. You can’t eliminate the chance of accidents, but you can reduce the risk you carry because of them.

It doesn’t have to keep you awake, though. If you’re a contractor who works with companies regularly, they will most likely have established standards of required coverage for you to get with your insurer and adjust to.

And if you’re hiring contractors… that’s what a tool like myCOI helps you do. We take the guesswork out of tracking certificates of insurance with powerful software and a team of insurance professionals who will ensure your COIs for construction are properly tracked.

Construction Liability Insurance Cost

What your construction liability insurance costs depends entirely on the size of your company, the kind of work you do, what your contracting company requires in the way of coverage, and who your insurer is. There isn’t a handy general liability insurance cost for contractors table, or a wall-mounted poster of subcontractor insurance costs.

Because insurance is the coverage of risk, your insurer will set their rates based on the variables of your company. A company with more employees has a greater potential risk than a company with one employee, just as a company that works indoors in a controlled environment carries less risk (usually) than a company whose employees work outside in random weather.

One risk the replacement cost of tools or materials. Do your employees work with dirt? That’s pretty inexpensive in most places. But if you’re using highly specialized equipment to work with rare or expensive materials, the cost of your risk is going to be higher.

Companies that hire you to work don’t want to assume that risk. That’s why they insist on certificates of insurance from you, so that you can shoulder the risk that you and your employees are generating.

One unique angle is the sole proprietorship; because they don’t have any other employees, figuring the independent contractor insurance cost becomes difficult.

Professional Liability Insurance For Contractors

Usually, contractors worry most about general liability insurance, for things like workers’ compensation or accident coverage. But more and more every year, more and more contractors are pursuing professional liability insurance for contractors. Now, what does professional liability insurance cover? Let’s take a look.

Professional liability coverage is different from general liability in that it covers professional services, their qualities, and their output. General liability insurance says you’ll pay for what you break; professional liability insures against you doing things wrong.

In the past professional liability was carried mostly by architects and designers, but as contractors take on more and more responsibility in the market, more business owners are telling their contractors professional liability claim scenarios are a real danger to think about.

Most insurers will now offer contractors professional liability insurance applications. Sometimes it is carried in parallel with similar coverage from the designers or architects, but as the line between contractor and designer continues to blur, this process will continue to change.

Construction Liability Insurance Policy

A good construction liability insurance policy will protect you and your company from claims damages or lawsuits during the construction process. For contractors, it’s a very common form of coverage to maintain, and something that those who hire contractors check carefully for when they’re verifying certificates of insurance. Construction liability insurance is protection from accidents or damages, unlike the prior example, professional liability insurance.

Sometimes a contracting entity will carry a project insurance policy as well, which may or may not overlap with a contractor’s construction liability insurance. Project insurance protects the whole project, rather than piecemealing out coverage to contractors or phases of the project. There are also forms of project insurance that protect against loss if a project is not completed or delivered.

Where the lines are drawn between these policies is where the necessity of careful monitoring and validation of certificates of insurance comes into play. Things like indemnifications, waivers of subrogation, and even who carries additional insured status will affect where the risk is placed in these projects.

Where the risk falls determines where the greatest cost falls, so all parties involved are wise to pay close attention. The course of construction insurance claims can be long and costly…

Who Sells General Liability Insurance for Contractors?

Answering the question “who sells general liability insurance for contractors?” is as easy as naming off all the top insurance providers. Almost every insurer will offer this kind of protection, though some vary whether they offer it nationally or locally. General contractors insurance is one of the most common forms of insurance.

You should check locally first, however. Or local to the area that you’ll be working, if you live near a state border and often work across the border. States require different types and levels of general contractor insurance requirements from businesses and contractors. It’s just good practice to check with the states you’ll be operating in; it’s not that uncommon, for example, for one state to require coverage that another state waives.

Putting in phrases like “general liability insurance for contractors near me” or “general liability insurance for contractors in texas” (if you live or work in Texas) is going to get you a list of the who’s-who of insurance providers. You’ll likely see names like GEICO, the Hartford, Next Insurance, or Hiscox Insurance in the top results.

Take the time to look at your local results, though. Dealing face to face with a local agent may provide you with a better experience than you’ll get filling out a faceless form on the internet.

Construction Insurance

By now you know construction insurance is not something you can ignore. No matter whether you’re a subcontractor, a general contractor, or a business that hires contractors or other third parties, construction insurance is a necessity. Leaving aside the legal requirements, it’s just good sense to protect yourself, your employees, and your business against unexpected risk and losses.

The exact kind of construction insurance you need depends on a lot of factors, as we’ve discussed. If you work in the homes market, you may need residential construction insurance. Building construction insurance requirements vary a great deal between residential and commercial projects, but the best construction insurance companies can help you navigate those differences with a minimum of fuss.

Remember again, though, requirements for insurance vary from state to state. Talk to your insurer, and if you’re a contractor, talk to your contracting entity to make sure you’re meeting their requirements of coverages. This is not something you want to rely on some form of “construction insurance for dummies” on.

General Contractor Insurance

General contractor insurance varies, like most insurance standards, very much from state to state, and depends very much on the structure of your business. Are you the sole proprietor of a one-person business? You’ll likely need less coverage than a contracting company that employs hundreds of contractors.

Think—and talk to your insurer—about the details of your business, too. Does your business own vehicles? You’re probably going to need to have some form of commercial auto insurance, which is going to add its own rules and premiums.

Do you have an office? Your leaseholder will almost certainly have requirements about the kind of coverage you need to protect that office space. Some states allow this to be covered with simple general liability insurance, but other states have more rigorous standards. Again: talk to your insurer, and check the laws and regulations in your state.

If you have employees, you’re almost certainly going to need to carry workers compensation insurance. The best general contractor insurance agencies can probably help you gain coverage for all of these kinds of insurance, but ultimately the responsibility lies with you.

And if you’re contracting contractors as third parties, you need to take extra care with your certificates of insurance. It’s not enough to just collect them. You need to make sure they’re valid, that they carry the coverages you require, and that you have a way to track and verify them.

myCOI can help with that.

Construction Insurance Coverage

Construction insurance coverage is a broad category, and it’s important that you figure out exactly where your company, project and required insurance fit into it. Insurance for construction workers is absolutely necessary, and not to be ignored or underestimated.

Remember, the details of the project and the people involved will dictate the kinds of coverage required. Construction project insurance can cover a lot, but it doesn’t cover everything. There are hundreds of guides to insurance for construction managers, don’t worry. It’s just a matter of selecting the correct one.

Your insurer is the best source of information about what kinds of coverage you might need. If you’re a contractor, you’ll also want to check with the business hiring you, to see what their standards are. And if you do different kinds of work for that company, make certain you check to see if the standards of coverage are different between projects!

Construction insurance coverage could be builder’s risk insurance or simple general liability insurance. Remember that it may include commercial auto insurance or even inland marine insurance for larger equipment. Don’t let the name fool you; inland marine covers more than just things that float!

Knowing what protections you need, and which are required of you by a contracting entity, is just part of the job.