Best Certificate of Insurance Tracking Software

Protect Your Business From Costly Claims

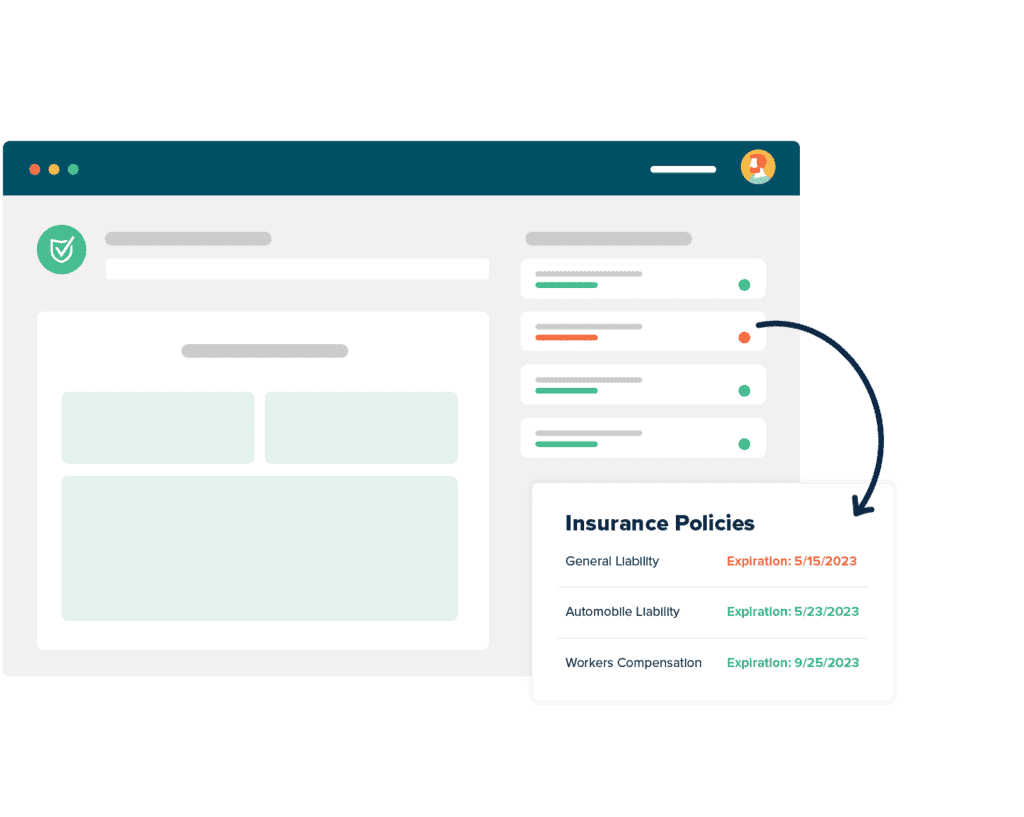

Ask your CFO or Risk Manager just how much claims and lawsuits can cost your business. If you are collecting certificates just to confirm they were received, you have no guarantee that your requirements are being met. myCOI Central is built on a foundation of insurance industry logic to ensure you remain protected with the appropriate coverage.

Automate Your COI Tracking

There’s no more need to worry about stacks of certificates cluttering up your office or hours of frustrating phone calls and emails to chase down certificates. myCOI Central provides your company with a solution to automate your insurance certificate requests, collection, and compliance resolution, while also giving your team a single, centralized repository to view compliance.

For Agents & Brokers

Win business and boost retention by providing agency branded, industry leading insurance tracking software to your insureds. Offer software only or add on your own compliance review services.

What Are The Benefits of COI Software?

What Our Customers Say

Certificate Of Insurance Template

The certificate of insurance (COI) might be one of the most critical items in a company’s risk management portfolio. It’s a simple form, but it carries a lot of weight. If you receive a certificate of insurance for business protection, for example, if you hire subcontractors and need those subcontractors to carry the insurance risk they generate through the course of their business, a COI is probably the mechanism by which you confirm that subcontractor is in fact carrying that protection.

Anyone can find an ACORD certificate of insurance sample. There are easily available PDFs anyone can fill out, and plenty of examples to show them what should go in each box. This small chance for fraud, limited as it may be, is just one of the reasons that companies like myCOI help companies just like yours track and verify the certificates of insurance that you receive.

Whether you’re a certificate holder who receives COIs or a named insured who provides them (we’ll explain those terms below!), knowing the ins and outs of a COI form is key. Let’s take a look.

ACORD 25 Certificate Of Insurance

As you are looking at your ACORD certificate of insurance example, and then double-checking your own actual certificate, it is important to make sure there are no mistakes. If you’re providing this certificate to a hiring entity, they’re going to verify your coverage. If there are discrepancies, that could slow down when you begin work or even delay the project.

Think of it this way: in many states, you’re required to carry a certificate of car insurance sample—well, not a sample, the little card your car insurance agent gives you is the actual certificate—in case you get pulled over, to prove you’re covered in case of an accident. Companies have to do the same check, except the insurance requirements for businesses when dealing with other businesses are far more complex.

If you’re learning how to read certificates of insurance, a sample ACORD 25 is a good place to start. It is the most common general liability certificate of insurance form, and the ACORD 25 instructions make it pretty easy to figure out, and you can find ACORD 25 PDFs pretty easy as well. A blank ACORD form is a great place to start.

On the ACORD 25 sample, there are a few common mistakes people make. One of the most common mistakes is getting policy numbers confused. Your auto, workers’ compensation, and general liability insurance policies may have different policy numbers. Make sure you pair the right policy number with the right type of insurance.

Furthermore, these policies may have different expiration dates. Do not assume they all have the same effective date and expiration date. If you do, you may end up assigning the wrong dates to the wrong policies. This will render your ACORD 25 form inaccurate. Double-check the policy effective dates and expiration dates before you provide the certificate to anyone. If you have questions about your insurance policies, reach out to your insurance provider for more information.

How To Verify A Certificate Of Insurance

Certificate of insurance compliance is the work a risk manager or compliance admin does to collect, verify and maintain the certificates of insurance provided to that company by its third parties: they are the experts who know how to verify a certificate of insurance for compliance.

Each certificate of insurance has to be checked, first and foremost to ensure that it represents all the necessary coverages, amounts, limits, and exclusions that your company requires of its contractors. Sure, there is general liability insurance mentioned, but does it protect to the same amount that you require?

Also, what assurances do you have that the contractor didn’t let the policy lapse the day after they handed you the COI? Are you verifying with insurance agents that these contractors still hold the policies and protections that their COI claims? Are there exclusions to the contractor’s protection that will mean you’re held responsible for risk that should properly rest with the contractor?

Remember that there are varied certificates of insurance requirements by state, and you need to be aware of them. Certificate of insurance best practices in every case remind you to check your state requirements, and we’d be remiss if we didn’t do the same.

Sample Certificate Of Insurance With Additional Insured

IRMI—the International Risk Management Institute—defines an additional insured as “a person or organization not automatically included as an insured under an insurance policy who is included or added as an insured under the policy at the request of the named insured.” That translates quite often as “I need to extend the coverage I purchase from my insurer to the third-party hiring me to do some work.”

A sample of additional insured endorsements is relatively easy to find online. A quick search will turn up a plethora of certificate of insurance additional insured wording. What you’re going to see is a standard certificate of insurance, but with the addition of the additional insured. Be careful that you don’t mistake a sample certificate of insurance with additional insured for an example of the kind of coverage you need to secure for your business; that’s a conversation you need to have with your insurer, not something you get from a PDF. A sample COI with additional insured is just meant to be an example of format.

ACORD Commercial Insurance

Ultimately, it is important for both large companies and contractors to make sure that they have the right commercial insurance. Plus, for every new business contract, it is important for contractors to make sure what is recorded on their ACORD general liability insurance certificate is enough to satisfy their hiring entity’s requirements. This insurance is important because it protects not only the client but also the contractor in the event that something happens to a worker or to the property during a job.

Furthermore, there are also situations where contractors may need to have something called an “additional insured.” Having this option means that the contractor is covered by general liability insurance and the policy also extends to certain other parties who may be involved in the same job, usually the entity hiring the contractor.

So no matter which form—or forms!—of insurance you have, it is important to display that proof of additional insured using an ACORD 25 additional insured form. Given how important this coverage is, anyone who has questions or concerns about how they should go about proving they have the right insurance policy should reach out to trained professionals to learn more. That way, you can rest assured that you have filled out the forms correctly and that you have all the best policies active for your business as well.

One mistake we often hear, though, is people looking for an ACORD insurance quote. Because of ACORD’s prominence in the industry, the uninformed sometimes confuse them for an insurer. ACORD does not issue policies or protections, only the standardized forms in use across the insurance industry.

Certificate Of Insurance For Business

When it comes to needing a certificate of insurance for business purposes, much depends on which business you are in that relationship. Let’s first look at when you’re the requesting business: you’re hiring contractors or vendors and you need to ensure they’re carrying the requisite coverage to shield your company from risk they create, without exclusions or limitations that your business won’t accept.

It almost goes without saying that you’re also on the lookout for fake business insurance templates or other attempts at fraud.

In this instance, you probably have either a tool like myCOI to help you with this, or you have a risk management checklist of some sort to check the certificates of insurance against. One common check is to decide whether your company needs to be just the insurance certificate holder vs additional insured; being endorsed as additional insured can extend coverage to your organization in the event of a loss or litigation caused by the third party you hire.

And if you’re on the other side, the contractor or vendor providing the certificate of insurance, all you really need to do is consult with your broker or other insurer, ensure you meet and can accept all the coverage requirements requested, and get an acceptable certificate of insurance issued by your broker.

ACORD Certificate Of Insurance Verification

The right form makes ensuring your vendors and contractors are in compliance much easier. With an ACORD certificate of insurance verification becomes a matter of confirming each of the listed values matches what your requirements are.

Easy, right? Not exactly. The easy and unquestioned access of anyone to free ACORD 25 fillable forms means that you may need to also verify the coverage with the issuing agent or broker. Knowing how to verify a certificate of insurance with the issuing agent is a handy skill for risk team members or compliance admins to have. Business insurance is a complicated business, and it pays dividends to learn all the skills you can.

Sometimes it’s not just coverage you have to verify. If you’ve held this certificate for a while, you may want to verify that the certificate is still valid. Coverage expires, or gets modified, and sometimes new certificates with accurate coverage are not provided to you.

Regardless, knowing how to verify a certificate of insurance is a skill every compliance admin or risk manager needs to know.